Ready to Defeat Your AML Compliance Obstacles?

Citadel Brings Revolution with Secure Solutions to AML Compliance Problems

A weak customer onboarding process can expose organisations to money laundering risks, regulatory penalties, and reputational damage.

Think of it like a security checkpoint at an airport: if checks are rushed or incomplete, the wrong people can slip through.

Several common gaps make the onboarding process vulnerable and reduce compliance effectiveness.

At the time of onboarding, when organisations fail to collect enough customer information, such as legal names, addresses, or source of funds, they may struggle to accurately identify customers and their business activities, creating compliance blind spots.

Verifying identity is a core part of customer onboarding, confirming that customers are who they claim to be. When these controls are weak, the result can be identity fraud, ML/TF risks, fines, and reputational damage.

Identifying the individuals who ultimately own or control an entity, a core part of Know Your Business (KYB) checks, is essential to enhancing transparency and reducing the risk of money laundering, sanctions evasion, or other financial crime.

Just as compliance is not one-size-fits-all, not all customers pose the same level of ML/TF risk. Effectiveness in risk assessment is important for identifying and mitigating potential risks and applying appropriate due diligence measures.

Customer risk profiles are dynamic and can change over time; conducting screening only at the time of onboarding creates significant vulnerability. Organisations should conduct ongoing monitoring, ensuring they remain compliant with regulatory expectations.

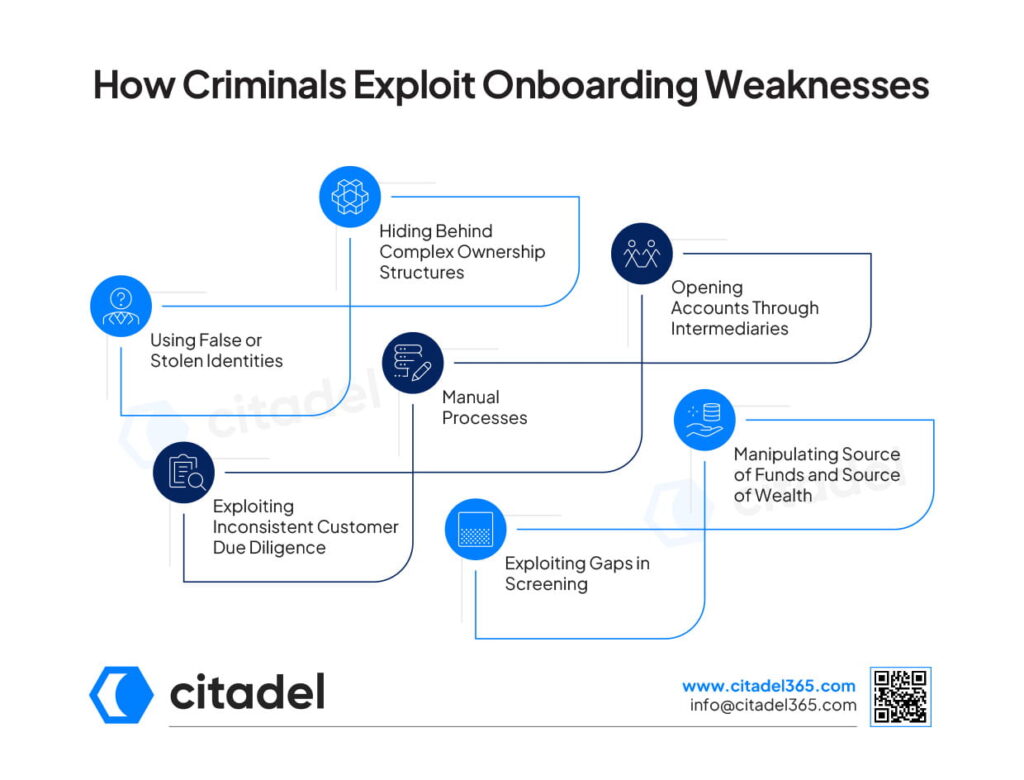

Customer onboarding is the first line of defence against financial crime; weak and uneven controls let criminals slip through, hiding their identities, masking ownership, and exploiting the financial system.

Using False or Stolen Identities

Criminals often use forged documents and stolen identities to bypass the verification controls, making it easier for them to enter the financial system.

Hiding Behind Complex Ownership Structures

Layered and complex ownership structures, including shell companies and nominee arrangements, can be used to conceal the true owner, and organisations may unknowingly onboard high-risk customers.

Exploiting Inconsistent Customer Due Diligence

Inconsistency in customer due diligence leads to gaps in the onboarding process that criminals might exploit, allowing them to evade detection and gain unauthorised access to financial services.

Manual Processes and Human Error

Manual processes can be vulnerable to oversight, human errors, and inconsistent decision-making, enabling criminals to exploit these weaknesses and circumvent compliance checks.

Opening Accounts Through Intermediaries and Third Parties

Third parties and intermediaries can be used to obscure the identity of the actual customer, making it difficult for organisations to identify the individuals ultimately controlling or benefiting from an account.

Exploiting Gaps in Sanctions and PEP Screening

Outdated and incomplete screening data allows sanctioned individuals or politically exposed persons (PEPs) to bypass the onboarding process and go undetected, increasing regulatory and reputational risks.

Manipulating Source of Funds and Source of Wealth Information

Criminals may also provide incomplete or incorrect information regarding the source of funds and source of wealth to disguise the illicit proceeds. Weak verification controls make it difficult to identify such misrepresentations.

Weak onboarding not only creates compliance gaps, but it also provides a gateway for financial crime. Weak onboarding results in various financial crimes, including:

Weak onboarding controls make it easier for criminals to introduce illicit funds into the financial system.

Weak screening and risk assessment processes can make it easier for individuals or organisations involved in terrorist financing to attempt to use legitimate financial services to transfer illicit funds.

Fraudsters may use stolen, fake, or synthetic identities to bypass verification controls during onboarding and conduct unauthorised transactions.

Sanctioned entities and individuals may try to conceal their true identities using third parties and intermediaries to access financial services due to weak screening controls.

Criminals may use trade-based money laundering techniques to disguise the movement of illicit funds. Common techniques include over/under invoicing or multiple invoicing.

Weak onboarding controls can enable mule accounts, which are used to transfer or receive illicit funds on behalf of others, and can increase the risk of account takeovers, where individuals gain unauthorised access to legitimate customers’ accounts.

Certain red flags may emerge after a customer relationship begins. The following key indicators suggest that important information was overlooked or insufficiently verified during onboarding:

Unusual transaction patterns, such as frequent high-value transactions right after the account opening, are inconsistent with the customer’s known profile.

Frequent updates to customer information, such as changes to addresses, contact details, or ownership structure, may indicate a red flag.

Unclear or vague information about the customer’s business activities may indicate elevated risk.

Unusual transactions that are inconsistent with the customer’s known profile or business income may indicate potential suspicious activity.

Adverse media and negative news linked to a customer can indicate elevated compliance risks and may suggest that important background checks were missed during onboarding.

Complex corporate and ownership structures with no clear stated purpose may indicate an attempt to conceal ownership, obscure the source of funds, or facilitate illicit activities.

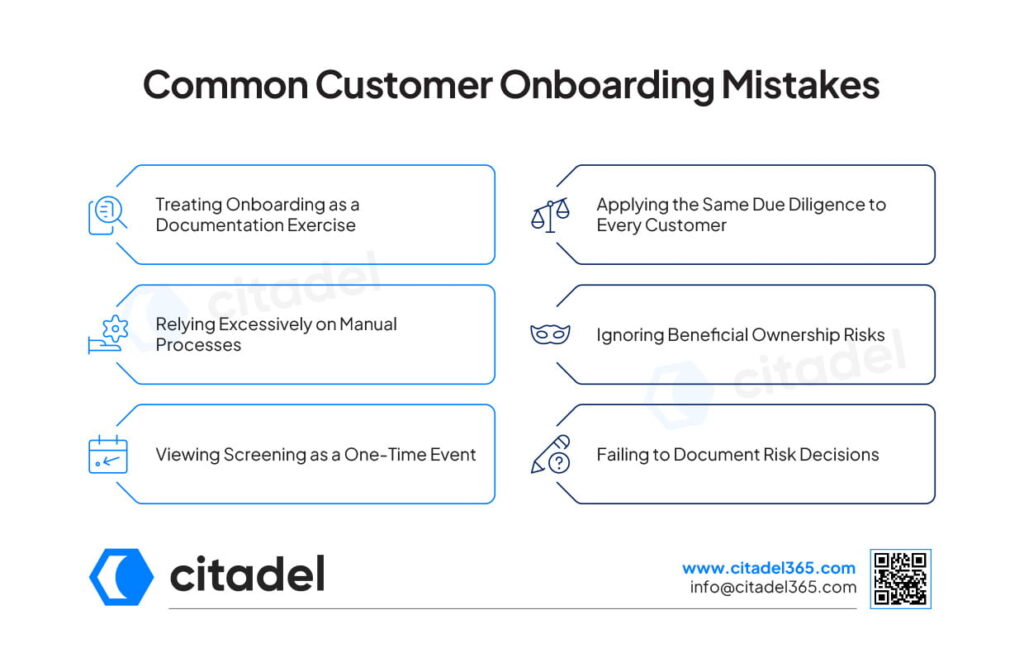

Common mistakes during the onboarding stage can lead to compliance gaps, increased ML/TF risks, and regulatory penalties. Some of the common mistakes include:

Treating Onboarding as a Documentation Exercise

Onboarding is not just about collecting documents; it is also about understanding the customer’s risk profile. Ignoring this can result in important red flags being overlooked.

Applying the Same Due Diligence to Every Customer

Applying the same due diligence for every customer may lead to insufficient scrutiny of high-risk customers and unnecessary effort for low-risk ones.

Relying Excessively on Manual Processes

Over-reliance on manual reviews increases the risk of human error, inconsistencies, and missed warning signs.

Ignoring Beneficial Ownership Risks

Failure to identify the ultimate beneficial owner (UBO) of a business can create opportunities for hidden ownership and increase the risks of ML/TF and other financial crimes.

Viewing Screening as a One-Time Event

Customer risks can change over time due to changes in customer information, sanctions lists, and watchlists. Conducting screening only once may leave emerging risks undetected.

Failing to Document Risk Decisions

Without the clear records and documentation of risk assessments and onboarding decisions, organisations may struggle to justify their actions during audits, investigations, or regulatory reviews.

A risk-based onboarding process significantly reduces the potential risks by tailoring the onboarding experience to the risk level posed by each customer.

Stronger Identity Verification

Verifying customer identities helps prevent fraud, identity theft, and the use of stolen credentials, which criminals use to access financial services.

Effective Customer Risk Assessments

Using a risk-based approach enables organisations to identify high-risk individuals, allowing them to allocate resources effectively and mitigate financial crime risks.

Comprehensive Screening Processes

Screening against sanctions lists, PEP databases, and adverse media helps detect customers with potential risks before onboarding.

Enhanced Due Diligence for High-Risk Customers

Applying enhanced due diligence for certain high-risk customers helps uncover hidden risks, suspicious ownership structures, and unexplained sources of funds that may indicate financial crime.

Ongoing Monitoring Throughout the Relationship

Continuous monitoring helps detect inconsistent customer behaviour, changes in risk profiles, and emerging risks, ensuring that potential risks are identified and addressed promptly.

Citadel365 strengthens customer onboarding by automating key compliance processes, supporting risk assessment, and helping organisations meet regulatory requirements.

Citadel365 streamlines customer information collection, helping organisations to gather and manage customer data efficiently while reducing manual efforts.

It also supports risk-based onboarding, enabling organisations to allocate resources effectively based on customer risk levels.

Citadel365’s automated screening against sanctions, PEPs, and adverse media lists, along with risk assessment processes, helps identify potential risks quickly and consistently at the time of onboarding.

Citadel365 helps maintain centralised, audit-ready customer records, enabling organisations to support compliance during regulatory reviews.

Criminals exploit customer onboarding processes to hide their identities, gain unauthorised access to financial systems, and conduct illicit activities.

Verifying beneficial owners is important to identify who ultimately owns or controls a business, often reducing the risk of hidden ownership and ML/TF risks.

Yes, weak onboarding can lead to sanctions breaches due to ineffective sanctions screening, allowing sanctioned individuals or entities to be onboarded.

Criminals often exploit poor CDD by providing false information, concealing beneficial ownership, or misrepresenting their activities to avoid detection.

Customer risk assessment helps organisations to identify high-risk customers and apply appropriate due diligence and monitoring measures.

Ongoing monitoring helps detect changes in customer risk profiles, identify suspicious activity, and surface emerging risks after onboarding.

Know Your Business (KYB) verifies a company’s legal existence, ownership, and control, while Know Your Customer (KYC) verifies an individual. KYB identifies ultimate beneficial owners and screens the business, its directors, and counterparties, which is essential when onboarding corporate customers.

Common money mule red flags include funds that leave an account almost immediately after they arrive, deposits from multiple unrelated sources, transactions that do not match the customer’s stated profile, and reluctance to explain the source of funds.

Screening is not a one-time event. Sanctions lists, PEP databases, and adverse media change constantly, so customers should be re-screened on an ongoing or periodic basis and whenever their information or risk profile changes. e-KYC and automated tools make continuous re-screening practical.

Arjun is the Co-founder and CEO of Citadel, where he leads the company’s vision across technology, business, and regulations. He brings over a decade of experience in building and scaling technology ventures. Arjun holds a B.Tech. in Information Technology and a Master’s in Management, supported by his certification as a Financial Crime Specialist, an uncommon combination that allows him to balance innovation with regulatory requirements.

Having advised leading banks and financial institutions on digital solutions and compliance technology, Citadel continues to grow with an ambition.