Ready to Defeat Your AML Compliance Obstacles?

Citadel Brings Revolution with Secure Solutions to AML Compliance Problems

Anti-Money Laundering (AML) alerts are signals generated by AML compliance software that indicate potential risk of financial crime, such as money laundering (ML), terrorist financing (TF), or proliferation financing (PF). The software generates AML alerts when customer behaviour or transactions differ from expected standards.

AML alerts are triggered during transaction monitoring, sanctions screening, PEP & adverse media screening, and changes in customer behaviours or risk profiles. The following points denote scenarios that trigger AML alerts:

Transaction Monitoring Alerts

Structuring patterns, unusually large transactions inconsistent with the customer profile, round-sum deposits or transfers, immediate funds deposit and withdrawal, sudden activity in an inactive or dormant account.

Sanctions Screening Alerts

Customer’s name exactly or partially matches individuals or entities on global sanctions watchlists such as OFAC and UN Consolidated Lists.

PEP and Adverse Media Alerts

The customer’s name matches an individual who holds a prominent public position, or their close associates (PEP), or is in adverse media.

Customer Behaviour and Risk-Based Alerts

Unexplained source of funds, transactions with high-risk jurisdictions or shell companies with no obvious business relationship, changes in beneficial ownership, and newly identified PEP status.

Such alerts may require internal review, escalation, or manual referral depending on their severity and the entity’s procedures.

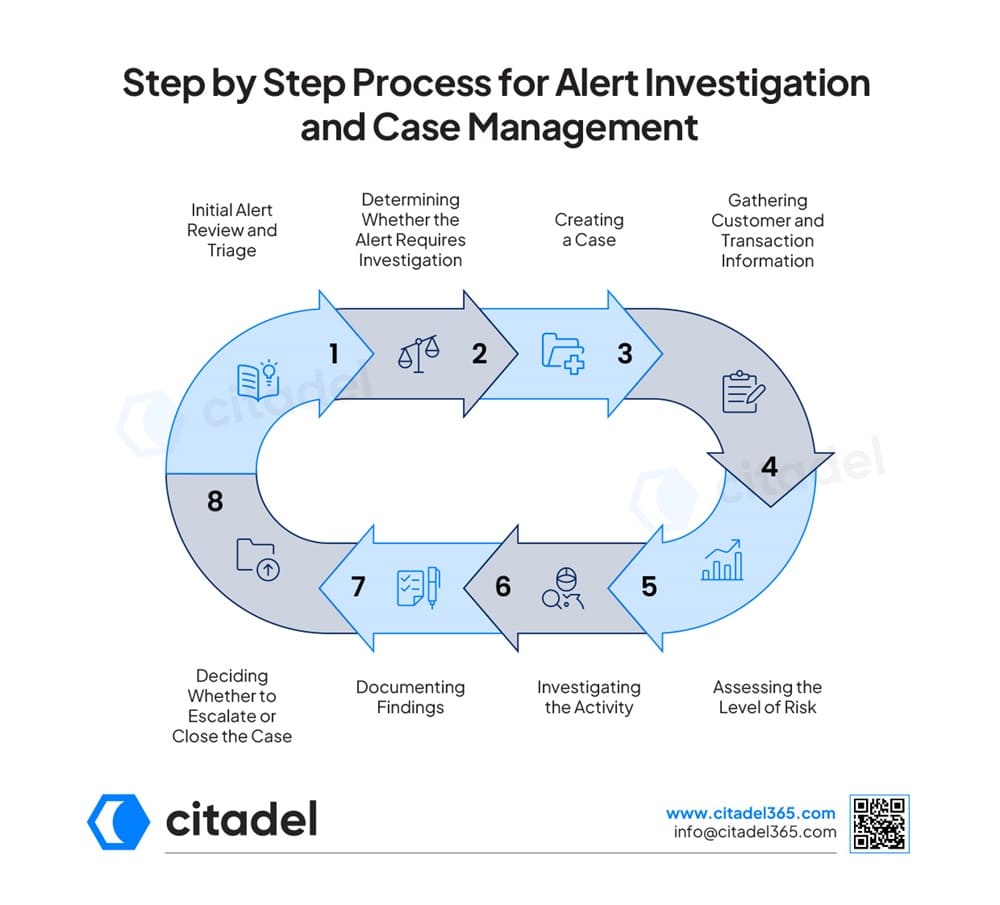

When an AML system generates an alert, the compliance team should verify the activity and determine whether it represents genuine suspicion or a false positive. The process involves:

An automated AML system flags a transaction or suspicious behaviour. The AML analyst checks the alert, understands what triggers it, and assesses risk and urgency.

The analyst investigates the alert and determines if it appears legitimate or a false positive.

Alerts that appear genuine require further investigation, for which a case must be created within the case management system.

The analyst gathers KYC records, transaction histories, account activity and supporting documents to establish a baseline of the customer’s normal behaviour.

The analyst evaluates the factors such as customer risk, geographic exposure, transaction behaviour, links to sanctions, PEP or adverse media.

The investigation involves a detailed analysis that determines whether the suspicious activity is consistent with the customer’s expected behaviour or indicates actual or potential ML/TF/PF risk.

The analyst documents the investigative steps, decisions, and conclusions drawn as an audit trail for regulatory compliance.

Based on the findings, the analyst closes the case if no suspicious activity is identified or escalates it for further review or for filing a suspicious activity report (SAR) or suspicious transaction report (STR) if suspicious activity is found.

Compliance teams investigate AML alerts by reviewing the customer’s profile to understand the baseline risk. The team screens the customer’s name against sanctions, PEP and adverse media lists. Further, the compliance team analyses the transaction patterns, including identifying structuring or other ML/TF techniques. Moreover, the compliance teams verify the source of funds and check counterparties as additional due diligence measures.

A false positive occurs when AML systems incorrectly flag a legitimate transaction or innocent customer behaviour as potential ML/TF activity. False positives may arise due to rigid thresholds, weak matching logic, poor data quality, duplicate customer records, or insufficient contextual information.

The investigator clears the alert when it matches the customer’s expected behaviour or known profile. Regulated entities must ensure a balance between managing risks and operational efficiency through tuning AML systems to reduce false positives. Also, even if the alert turns out to be a false positive, it still requires thorough checks to ensure its legitimacy and support regulatory compliance.

When suspicion remains even after the compliance teams have investigated the legitimacy of the transaction or customer activity, the following steps should be taken:

An AML investigation concludes the following:

Compliance teams face the following challenges while investigating AML alerts:

Citadel365 provides compliance teams with a single platform to manage alerts. Its case management software allows compliance teams to manually create a case and define the reason for review. Further, it allows prioritising cases based on their risk level, enabling teams to focus on high-risk activities.

Citadel365 unifies alerts, customer data, and transaction records to ensure transparency, support decision-making, and strengthen investigation workflows. The software facilitates collaboration by enabling teams to assign responsibilities and share information on a common platform.

Citadel365, with cloud storage, provides a centralised space for documentation, improving visibility. Moreover, its effective audit trails ensure every action is recorded to demonstrate compliance during regulatory reviews or audits and ease reporting.

No, an AML alert does not mean suspicious activity has been confirmed. It is an AML system flagging a customer activity or transaction that may be indicative of ML/TF risks based on predefined rules or thresholds.

An alert is an automated notification generated on an AML system that may indicate financial crime, while a case is created to investigate, track and resolve an AML alert.

Yes, AML alerts may result in Suspicious Transaction Reports (STRs) if the customer is found suspicious on reasonable grounds of money laundering or other financial crime.

An AML alert that results in a false positive should be dismissed during investigation. Compliance teams should tune their system rules and thresholds to reduce false positives.

Case management provides a centralised space to create, prioritise, review, resolve, track, close and document a case for AML investigations, helping compliance teams automate workflows, collaborate and stay audit-ready.

Arjun is the Co-founder and CEO of Citadel, where he leads the company’s vision across technology, business, and regulations. He brings over a decade of experience in building and scaling technology ventures. Arjun holds a B.Tech. in Information Technology and a Master’s in Management, supported by his certification as a Financial Crime Specialist, an uncommon combination that allows him to balance innovation with regulatory requirements.

Having advised leading banks and financial institutions on digital solutions and compliance technology, Citadel continues to grow with an ambition.