Ready to Defeat Your AML Compliance Obstacles?

Citadel Brings Revolution with Secure Solutions to AML Compliance Problems

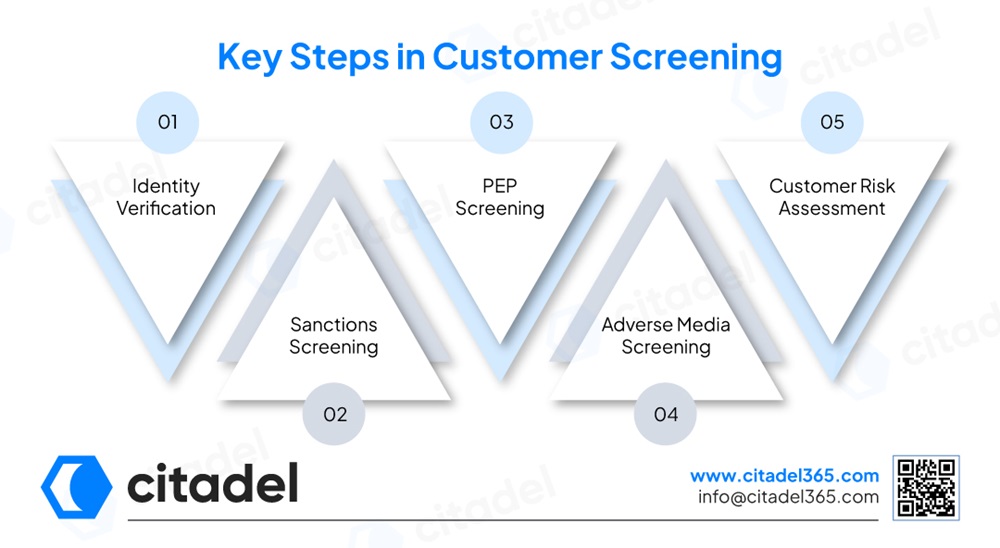

Regulated entities collect customers’ information to verify that the customer is who they claim to be.

Checks the customer against the government or international watchlists, such as the UN Consolidated Lists and the UAE Terrorist Lists, to prohibit establishing business relationships with sanctioned individuals/entities.

Identify if the customer holds a prominent public position or is a close relative of a PEP by checking against PEP global databases.

Checks customers against negative news to identify individuals or businesses involved in financial crime.

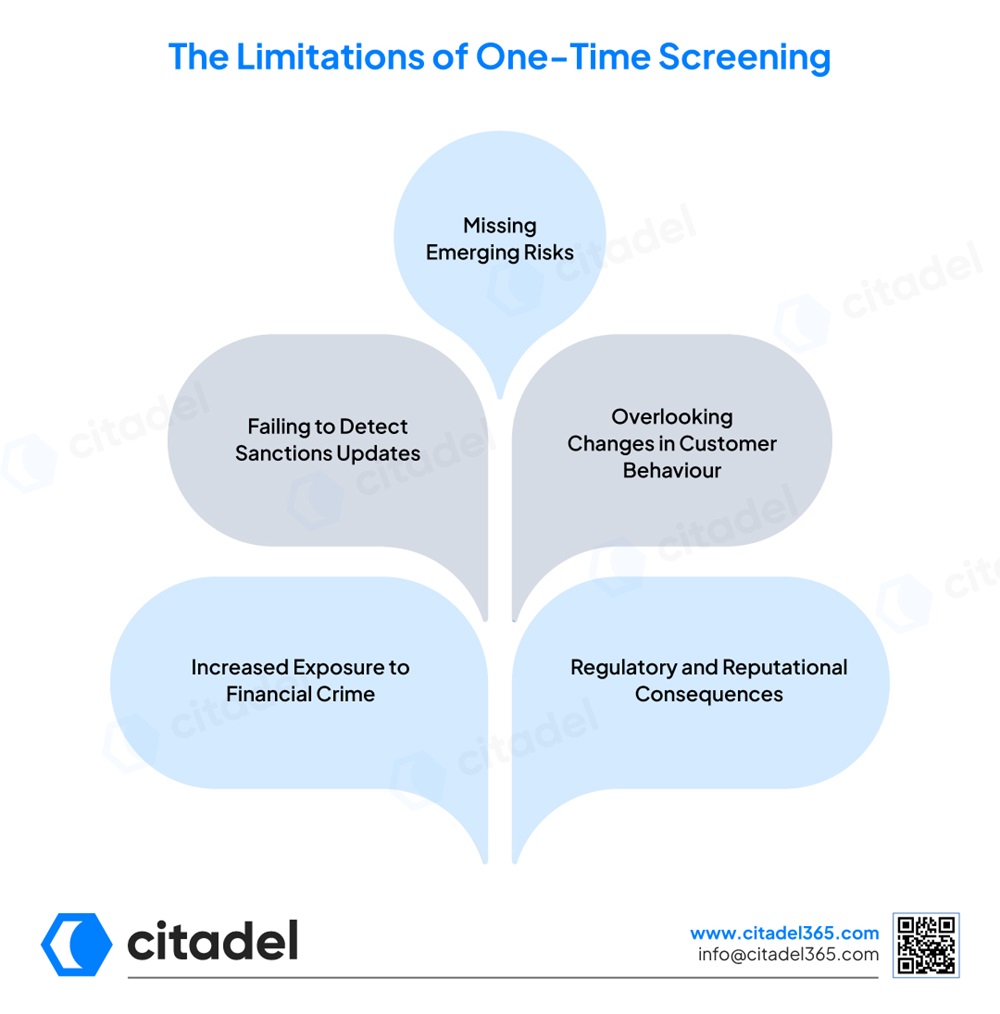

Regulated entities that perform one-time screening and not periodic checks may expose themselves to sanctions, regulatory penalties, or reputational damage.

Missing Emerging Risks

As financial crime and global watchlists evolve constantly, one-time screening may miss emerging ML/TF risks, leading to regulatory penalties.

Failing to Detect Sanctions Updates

An individual or entity customer who’s at low risk may become sanctioned; one-time screening fails to detect such changes.

Overlooking Changes in Customer Behaviour

Sudden changes in customer behaviours, such as frequent small transactions to high-risk jurisdictions or sanctioned individuals, are often ignored with one-time screening.

Increased Exposure to Financial Crime

Regulatory and Reputational Consequences

Regulators expect screening to be an ongoing process, and failure to comply with regulatory expectations may result in financial penalties, criminal liability, and reputational damage.

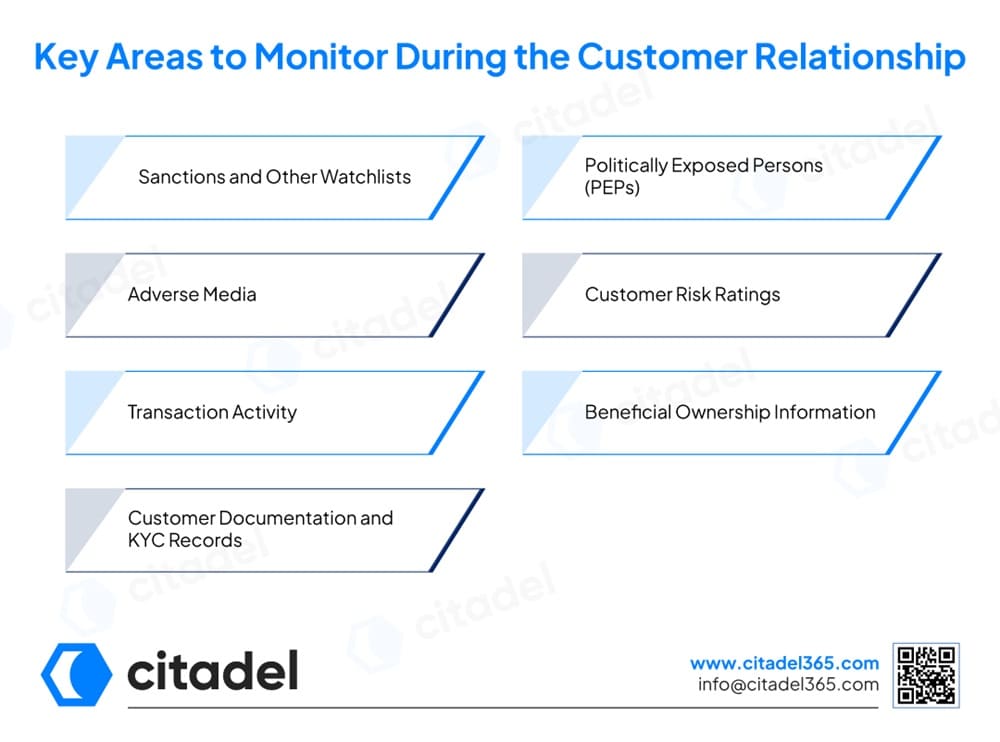

Regulated entities should monitor customers against sanctions watchlists, PEP databases and adverse media sources. It helps them assess risk appropriately, apply enhanced due diligence, and prohibit sanctions exposure.

Further, entities should review the customer risk ratings periodically to keep the customer risk profile updated with changes in customer behaviour and their status.

Moreover, ongoing transaction monitoring helps identify unusual patterns and large volume transactions to high-risk jurisdictions that may indicate ML/TF risks. Regulated entities should keep beneficial ownership information accurate and updated when an ownership structure changes.

Additionally, regulated entities should monitor identification documents and KYC records to keep them current and ensure compliance with regulatory requirements.

Regulated entities should adopt a risk-based approach to ensure that screening frequency aligns with the customer risk. Regulatory authorities expect regulated entities to keep customer information up to date and identify risk in real-time.

Customer re-screening occurs during significant events, for instance, changes in ownership, sanctions list, customer behaviour, PEP status or adverse media findings. Further, customers with high-risk, such as PEPs, complex ownership structures, require increased monitoring or re-screening, compared to low-risk customers.

Regulated entities should use automated screening solutions for continuous and real-time monitoring of customer details against global watchlists and ensure compliance with AML requirements.

Regulated entities should avoid the following mistakes to prevent financial crime and ensure AML/CFT compliance:

Citadel365 allows automated name screening against sanctions, PEP and adverse media lists to help regulated entities identify customer risks and ensure AML compliance. Further, the software facilitates continuous monitoring throughout the customer lifecycle rather than one-time checks to assess risks when customer profiles change.

Citadel365 customer risk assessment software automatically calculates onboarding risk using parameters such as nationality and customer type, including screening risks and enables dynamic risk scoring.

Citadel365 helps reduce false positives by allowing configured thresholds and risk-based logics to filter out low-risk matches. Moreover, its case management software provides a single platform for managing compliance workflows, thereby improving operational efficiency and reducing human errors. Its audit-ready records enhance regulatory reporting and ensure compliance with AML/CFT regulatory requirements.

Customer risk profiles and global sanctions watchlists are constantly evolving, requiring regulated entities to conduct ongoing screening to comply with regulatory requirements.

Regulated entities must re-screen customers based on their risk level and regulatory requirements. AML software such as Citadel365 performs ongoing screening to identify changes in sanctions, PEP status and adverse media individuals in real time.

Factors such as changes in customers’ risk profiles, document expiry, PEP or adverse media status, corporate structure changes, and transactions to unexpected parties trigger ongoing customer monitoring.

When new sanctions are introduced, regulated entities must perform re-screening to identify whether existing customers, beneficial owners, or counterparties are not included in the sanctions list. It helps regulated entities understand risks in real time and apply measures quickly to remain compliant.

Yes, using software solutions such as Citadel365, which provides a centralised platform to screen customers against sanctions, PEP and adverse media in real-time, customer screening can be automated.

Arjun is the Co-founder and CEO of Citadel, where he leads the company’s vision across technology, business, and regulations. He brings over a decade of experience in building and scaling technology ventures. Arjun holds a B.Tech. in Information Technology and a Master’s in Management, supported by his certification as a Financial Crime Specialist, an uncommon combination that allows him to balance innovation with regulatory requirements.

Having advised leading banks and financial institutions on digital solutions and compliance technology, Citadel continues to grow with an ambition.