Ready to Defeat Your AML Compliance Obstacles?

Citadel Brings Revolution with Secure Solutions to AML Compliance Problems

A customer risk score is a compliance measure used to assess a customer’s risk exposure to money laundering and terrorist financing, supporting a risk-based approach by assigning a risk level based on factors such as customer profile, geographic area, delivery channel, products/services and transactions.

Businesses use risk scoring to ensure they allocate compliance resources effectively, categorise customers based on risk level, support customer due diligence, enhance due diligence, and enable institutions to monitor and prioritise high-risk customers more effectively, rather than treating all risks the same.

The customer risk scores are categorised into Low, Medium, and High-risk categories based on various factors.

Risk scores and risk ratings serve different purposes within an AML framework. A risk score is a numerical representation of risk calculated based on predefined AML risk factors, whereas risk ratings are a systematic method of classifying risks into low, medium, and high-risk categories.

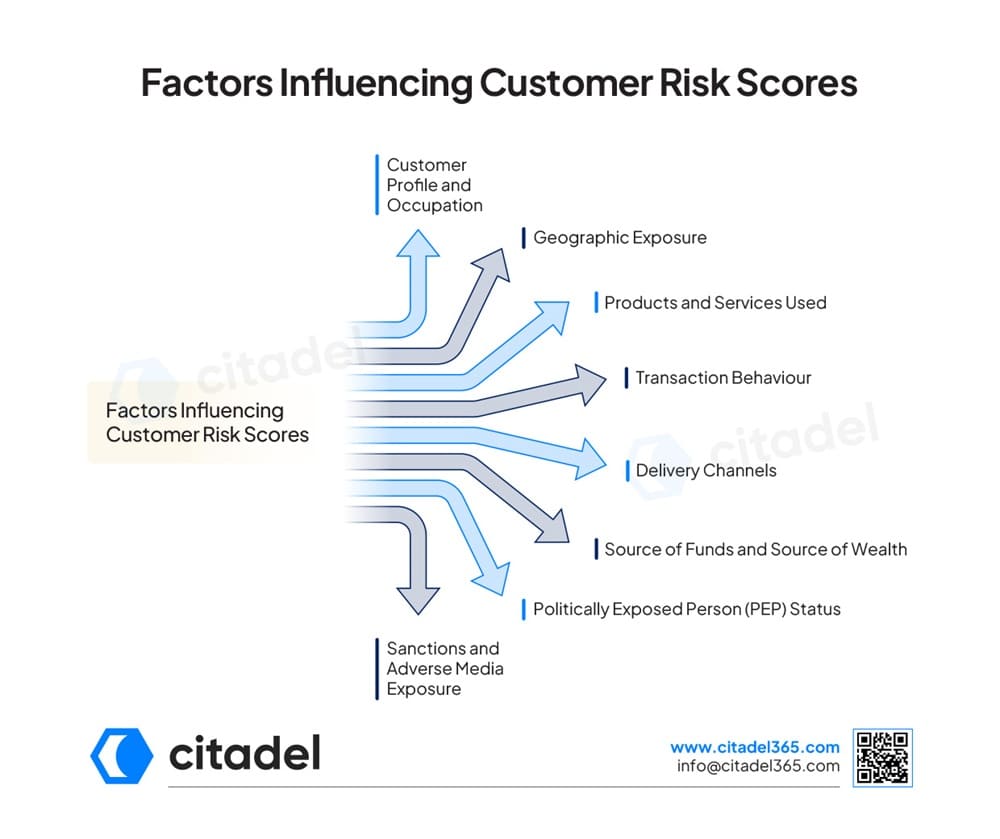

Customer risk scores are influenced by various factors. Here is the breakdown of key factors that can impact a customer’s risk score:

Customer type, occupations, and business activity can influence risk levels, as certain industries may present higher exposure to financial crime.

Geographic exposure, including connections to high-risk jurisdictions and to sanctioned countries, may increase the customer’s risk score.

Some of the high-risk products and services may also influence the risk score, particularly those involving complex structures, cross-border, or high-value transactions, which can elevate the ML/TF risks.

Unusual or inconsistent transaction behaviours may indicate increased ML/TF exposure, often impacting the risk scoring.

Mediums such as non-face-to-face onboarding, digital channels, and the use of third-party intermediaries can increase ML/TF risks due to a lack of transparency.

Understanding the customer’s SOF and SOW is essential for assessing legitimacy; an unclear source of funds or wealth can increase risk scores and trigger due diligence requirements.

Customers identified as PEPs, including their family members and close associates, pose higher ML/TF risk and require increased monitoring and enhanced due diligence.

Exposure to sanctions or adverse media can significantly elevate a customer’s overall risk profile.

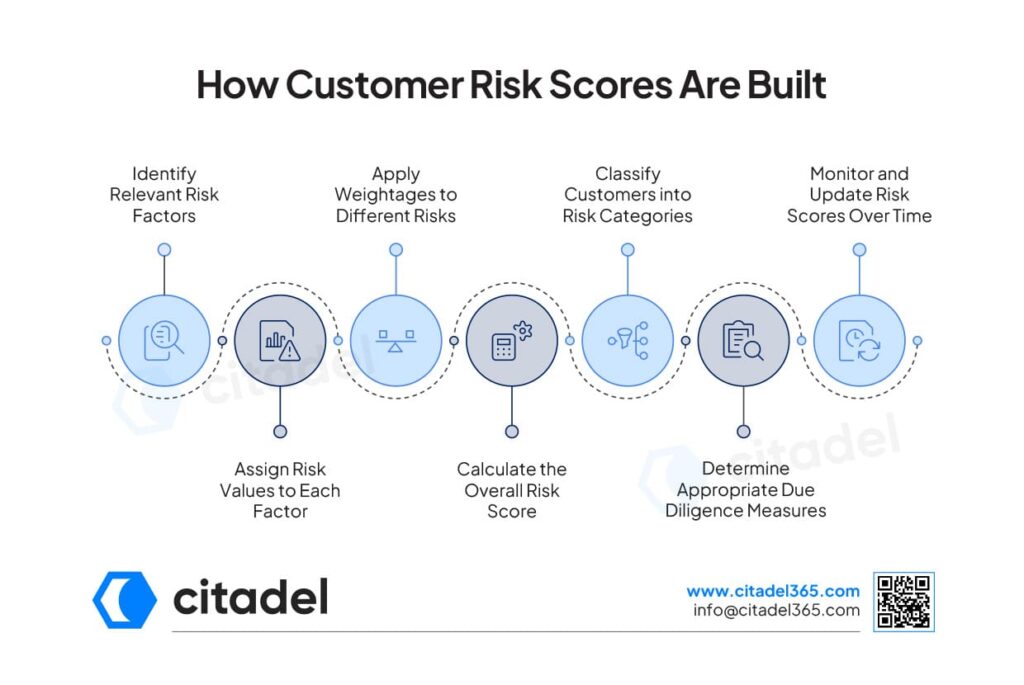

The process of building the customer risk scores involves several key steps that enable institutions to assess and manage ML/TF and other financial crime risks.

Identify Relevant Risk Factors

Identify and define relevant risk factors that will be used to assess customers’ overall risk profile, such as customer type, geographic location, products and services used, transaction behaviour, and delivery channel used.

Assign Risk Values to Each Factor

Assign numerical risk values to each factor based on the inherent risk level it presents, such as customers from high-risk jurisdictions may receive a higher score than those from low-risk jurisdictions.

Apply Weightages to Different Risks

Apply weightages to reflect the importance of each risk factor; factors with greater ML/TF risk impact should carry a higher weightage in the scoring model.

Calculate the Overall Risk Score

After assigning risk values and weightages, calculate the overall customer risk score that reflects the customer’s total risk exposure.

Classify Customers into Risk Categories

Map the calculated risk score to predefined risk categories of Low, Medium, or High Risk, making it easier for compliance teams to understand and act on the results.

Determine Appropriate Due Diligence Measures

Once the customer’s risk category is established, appropriate due diligence measures can be applied.

Monitor and Update Risk Scores Over Time

A customer’s risk profile can change over time due to new transactions, changes in business activities, or shifts in geographic exposure. Ongoing monitoring ensures that the risk assessment remains accurate and up to date.

Customer risk scores should be dynamic and not static, as customer information, behaviour, and risk exposure keep changing over time; that’s why risk scores must be updated to ensure risk assessment remains accurate and relevant.

Customers and Risks Change Over Time

Changes in customers’ activities, business relationships, or geographic exposure can change the overall risk profile, requiring their risk score and rating to be reassessed.

New Information Can Affect Risk Ratings

New information, such as changes in sanctions lists, unusual transactions, new geographies, or adverse media alerts, can significantly impact the customer’s risk rating.

Behavioural Changes May Trigger Reassessment

Behavioural changes, including unusual transaction patterns or activities inconsistent with the customer’s known behaviour, may require a risk reassessment.

Continuous Monitoring Supports Accurate Risk Profiles

Ongoing monitoring helps organisations to identify evolving risks and maintain updated risk assessments throughout.

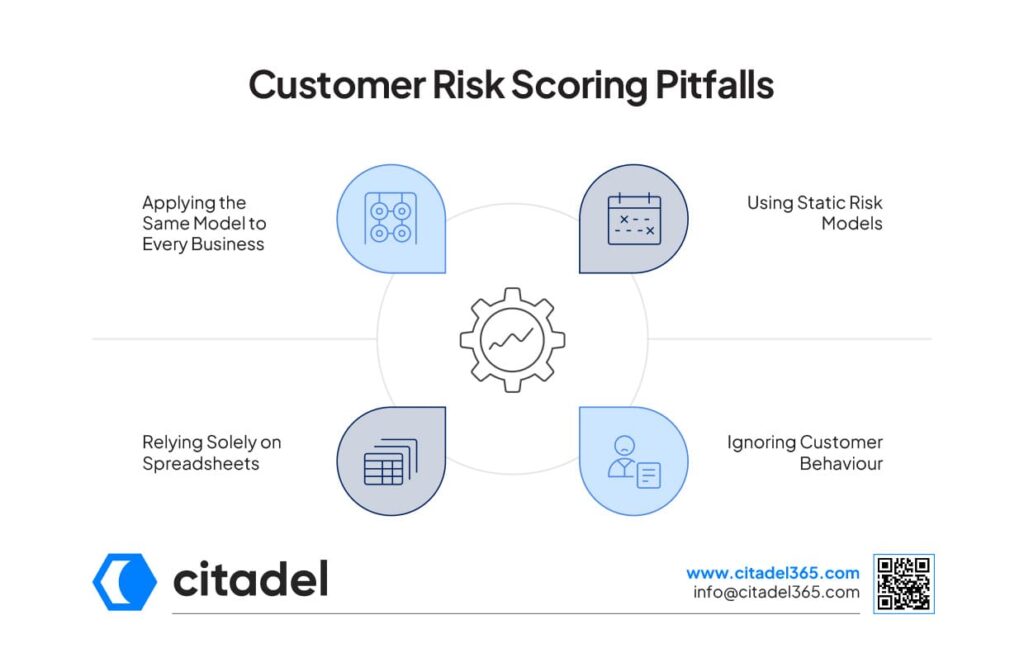

The common mistakes that businesses make when building customer risk scores are as follows:

No one-size-fits-all risk scoring models. A framework that is suitable for one organisation may not work for another due to changes in customers, products, services, and risk exposure.

Risk profiles change over time, risk models that are not reviewed regularly and updated may fail to reflect changes in customer information, behaviour, or evolving risks.

Ignoring customer behaviour such as inconsistent transaction patterns and changes in customer activity may result in inaccurate risk assessment and missed red flags.

Dependency on spreadsheets often requires manual data entry, increasing the risk exposure. Automated risk scoring often improves accuracy and consistency.

Citadel365 helps in building smarter customer risk scores through its configurable risk methodologies and applies weightage-based risk scoring to generate more accurate risk scores.

Citadel365 ensures dynamic customer risk profiles, keeping them up to date as information, activities, and risk indicators change.

The software also automatically classifies customers into predefined risk categories based on their risk scores and enables continuous monitoring to identify the changes that may impact customers’ risk profiles.

Citadel365 maintains a clear audit trail of risk assessments, scoring methodologies, and decisions made to support regulatory investigations.

Businesses assign different weightages to reflect the relative impact of each risk factor on the customer’s overall risk profile.

A risk score is a numerical value, while a risk rating is the category assigned based on that score.

Yes, customer risk scores can change over time due to changes in information, transaction activity, or changes in risk exposure.

Customer risk scoring is important in AML compliance to identify high-risk customers, prioritise them, and support regulatory compliance.

Yes, automated systems like Citadel365 can calculate, update, and monitor risk scores effectively while supporting ongoing compliance.

Arjun is the Co-founder and CEO of Citadel, where he leads the company’s vision across technology, business, and regulations. He brings over a decade of experience in building and scaling technology ventures. Arjun holds a B.Tech. in Information Technology and a Master’s in Management, supported by his certification as a Financial Crime Specialist, an uncommon combination that allows him to balance innovation with regulatory requirements.

Having advised leading banks and financial institutions on digital solutions and compliance technology, Citadel continues to grow with an ambition.