Ready to Defeat Your AML Compliance Obstacles?

Citadel Brings Revolution with Secure Solutions to AML Compliance Problems

AML software for fintechs and payment service providers in the UAE is an automated tool that helps them detect and prevent financial crimes. It helps UAE fintechs comply with core AML obligations, including customer due diligence, identity verification, and anomaly detection.

UAE fintechs and payment service providers require faster customer onboarding as customers expect accounts to be opened within minutes. On the other hand, regulators expect strong anti-money laundering controls. Institutions that rely on manual compliance processes cannot keep pace with increasing transaction volumes and often delay onboarding.

AML software automates KYC with liveness checks, performs real-time screening, assesses risk scores, identifies mule accounts, and prioritises alerts.

The Central Bank of the UAE (CBUAE) is the primary supervisory authority that supervises fintechs in the UAE. The authority oversees payment activities such as stored value facilities, payment aggregators, retail payment services, and e-money issuers.

The CBUAE expects fintechs to implement an AML/CFT framework, including digital CDD as effective as branch onboarding, system oversight based on transaction frequency, volume and customer profiles, and active systems that help detect & prevent financial crime.

AML software helps fintechs meet regulatory expectations by automating compliance procedures. It helps them verify customer identities, check them against a global watchlist and assign risk scores based on customer behaviour and profile.

UAE AML Requirement | Sector Challenge | AML Software Feature | Evidence Generated |

Digital CDD | Remote identity verification at speed and scale | KYC self-service with document capture and liveness check | Customer profile, liveness record, ID documents |

Liveness Verification | Confirming a real person behind a digital application | Liveness check integrated into onboarding flow | Liveness verification record, timestamped |

Sanctions Screening | Real-time screening at application and ongoing | Real-time sanctions, PEP, adverse media screening | Match results, alert notes, review history |

Risk Assessment | Automated scoring at onboarding and ongoing | Configurable risk models with automated EDD triggers | Risk scores, rationale records |

Mule Detection | Identifying mule and funnel account patterns | Behavioural risk scoring and transaction pattern alerts | Mule pattern alerts, investigation trail |

Alert Management | High-volume alert triage at digital scale | Risk-based alert prioritisation and case management | Alert records, triage logs, decision notes |

STR/SAR Support | Fast STR preparation for fintech reporting timelines | Case management with goAML STR preparation workflow | Investigation notes, escalation records |

Ongoing Monitoring | Daily rescreening and behavioural monitoring | Automated rescreening and rule-based monitoring | Rescreening logs, monitoring alerts |

AML software helps fintech and payment service providers detect the following red flags that indicate money laundering, terrorist financing or other financial crime:

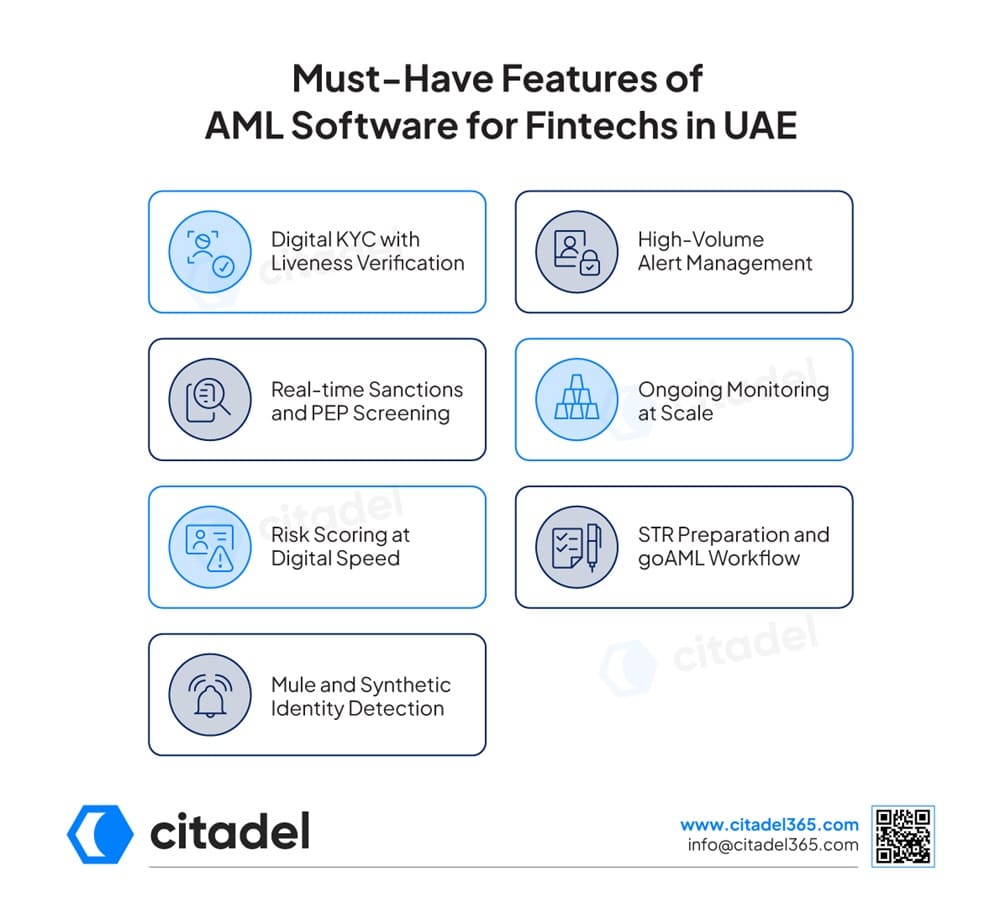

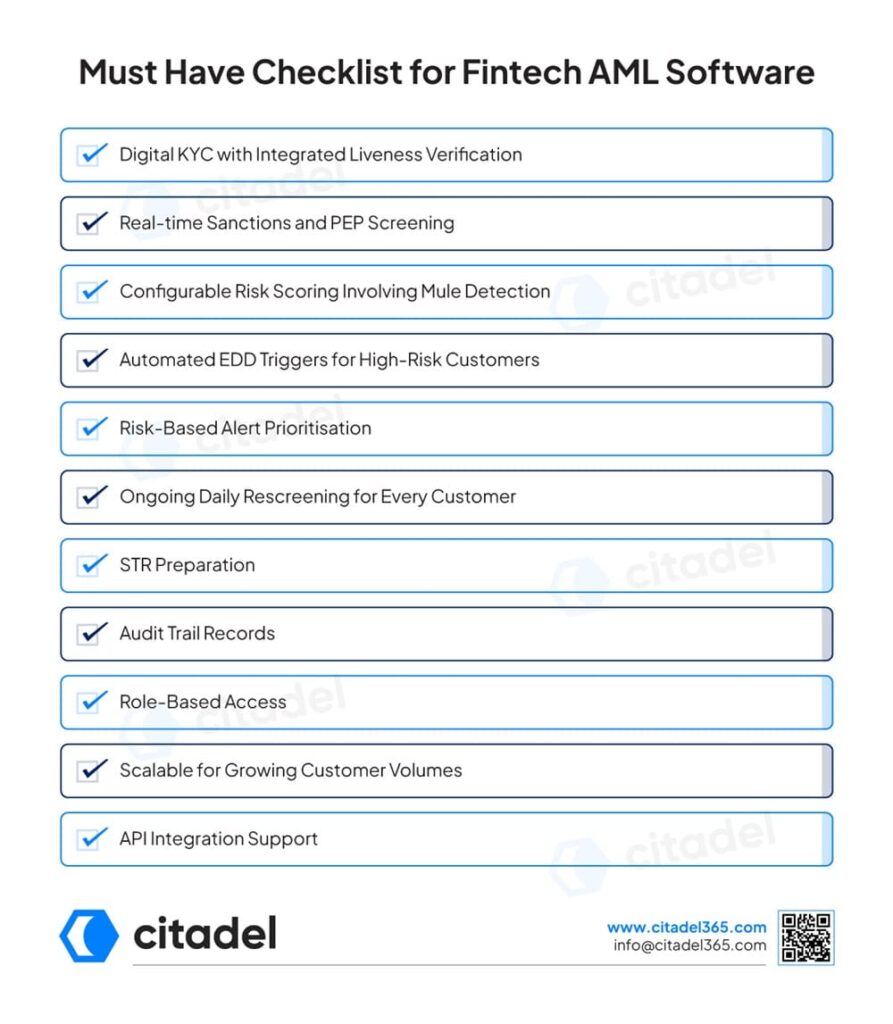

The AML software should integrate the following features for fintechs to meet regulatory obligations and streamline compliance processes:

AML software should support a self-KYC service with document capture and liveness checks. It should automate identity verification rather than manual checks, which removes delays and enables faster onboarding.

Fintechs require AML screening software that instantly checks customers against global sanctions watchlists and PEP lists. AML software should allow automated name screening against the sanctions lists and PEP databases during onboarding. The software should also perform real-time screening and ongoing watchlist monitoring for onboarded customers to flag matches and generate alerts.

AML software should evaluate a customer’s behaviour at onboarding and update their risk profile when the behavioural patterns change. It should allow fintechs to configure risk scores in line with business policies, helping compliance teams to focus on high-risk customers.

AML software should identify suspicious accounts by evaluating customer behaviour and transaction patterns. It should detect mule accounts and synthetic identity fraud, allowing compliance teams to begin an investigation and report suspicious activity promptly.

Effective AML alert management means the system should sort alerts by priority so compliance teams can focus on high-priority cases first. Instead of manually reviewing every alert, the AML software should help instantly filter out false alarms and help speed up investigations. For instance, an alert that a client is a sanctions match should be denoted as high-risk rather than a small increase in transaction volume, which can be treated later.

AML software should perform daily rescreening for every customer to automatically check them for changes in their risk profile. This may include a change in customer status and generate an automatic alert accordingly. Continuous transaction monitoring complements rescreening by flagging unusual payment activity as it happens.

Fintechs are required to file a suspicious transaction report (STR) for suspicious transactions. AML software should help the compliance team prepare STRs by centralising case information, making it easier for them to review cases, prepare reports, and file reports through the goAML platform.

Citadel365 is a centralised AML platform that helps fintechs and payment service providers streamline compliance processes to meet UAE AML/CFT regulations. It automates identity checks and helps firms to initiate onboarding with minimal initial data. Further, the self-KYC feature helps speed up customer onboarding and enhance the user experience.

Citadel365 performs name screening to detect sanctions, PEP, and adverse media matches in real-time. Moreover, the software automates risk scoring and helps update customer risk profiles with customised settings.

Citadel365 monitors transactions to detect anomalies and manages high-volume alerts to reduce alert fatigue. Additionally, it helps fintech platforms, e-money issuers, payment aggregators, retail payment service providers, and stored value facility operators with audit-ready compliance records through effective audit trails, supporting decision-making and regulatory reporting.

Fintechs must ensure that the AML software has the following components:

Furthermore, fintechs and payment service providers should ask the following questions to the AML software vendor:

AML compliance for fintechs and payment service providers in the UAE involves digital onboarding, requiring them to conduct accurate KYC and screening to comply with AML regulations. AML software helps fintechs and payment service providers with identity verification, integrating liveness checks, real-time sanctions & PEP screening, risk scoring, anomaly detection, alert management, and ongoing monitoring.

Fintechs in the UAE are supervised by the Central Bank of the UAE (CBUAE), which ensures they comply with AML obligations and may impose penalties for non-compliance.

Liveness verification, or liveness detection, is a security check that analyses facial movements and features to ensure that a real person is operating a device. UAE fintechs require liveness verification during remote customer onboarding to help protect against risks of deepfake impersonation or synthetic fraud.

AML software detects mule accounts by monitoring transaction patterns, customer behaviour, and device information. It helps fintechs identify unusual fund movements, frequent transfers, and anomalies that indicate an account used by criminals to transfer illicit funds.

Real-time screening means checking customer and transaction data as they occur, while batch screening processes large volumes of data at fixed intervals, which can delay risk detection.

Yes, Citadel365 supports CBUAE compliance for payment service providers (PSPs) by automating digital onboarding, real-time sanctions and PEP screening, assessing risk scores, and providing audit-ready compliance records.

Sridhar is a Certified Anti-Money Laundering Investigator (CAMI) with over 30 years of experience in compliance, risk, and audit, including more than 20 years in AML and financial crime prevention. He has contributed to the development of UAE regulatory standards through the FERG sub-committee and has maintained active engagement with the Central Bank of the UAE on supervisory and compliance matters.