Ready to Defeat Your AML Compliance Obstacles?

Citadel Brings Revolution with Secure Solutions to AML Compliance Problems

Source of Funds (SoF) refers to the origin of money that an individual or entity uses to conduct a transaction. Regulated entities in the UAE validate SoF to trace the flow of funds and verify that they were obtained legally. Source of Funds verification is a defence used by regulated entities to detect and combat money laundering (ML), terrorism financing (TF) and other financial crime.

The source of funds helps regulated entities determine where the money for a particular transaction came from and how it reached a specific account. Cabinet Resolution No. 134 of 2025 mandates Financial Institutions, DNFBPs and VASPs in the UAE to verify SoF, especially for high-risk customers.

Source of Wealth (SoW) provides an overview of a customer’s financial status. It involves the long-term history and activities that summarise how the customer acquired the assets. The source of wealth checks is necessary to understand how a person acquires overall wealth and assets across their lifetime and ensure that their wealth is consistent with their background and income sources.

Regulated entities in the UAE should check the source of Wealth as part of Enhanced Due Diligence, as mandated under Cabinet Resolution No. 134 of 2025. For instance, for high-risk clients such as PEPs, SoW checks are essential to prevent financial crime.

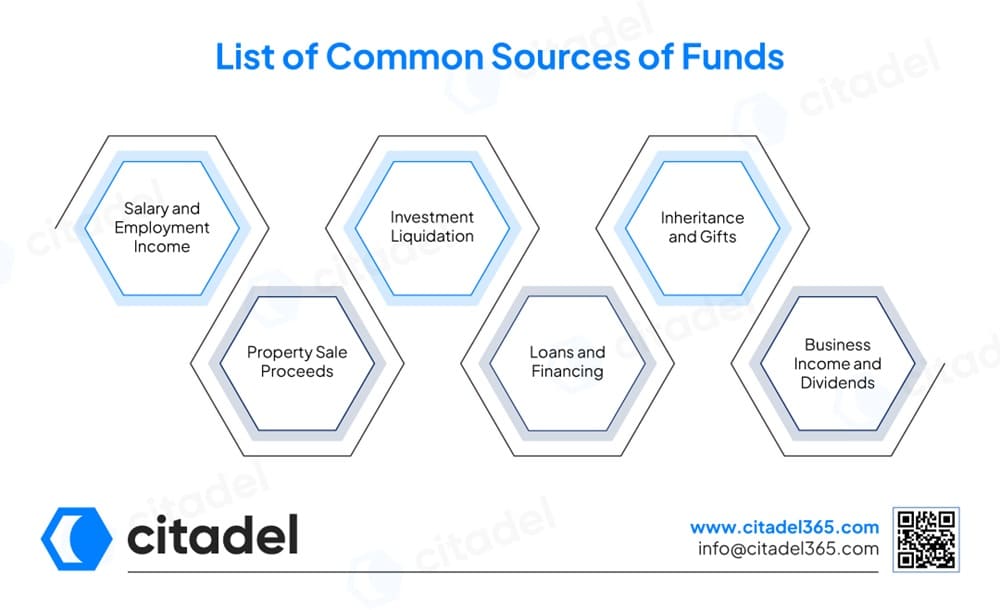

Some of the common sources of funds include salary and employment income, property sale proceeds, investment liquidation, loans and financing, inheritance and gifts, and business income and dividends. Regulated entities verify the reasonable or contributing sources among them to ensure funds are legitimate.

The entities verify the following documents to check the source of funds legitimacy:

The common sources of wealth (SoW) include long-term business ownership, investment portfolios, inherited wealth, real estate holdings, professional & employment income, and family wealth & asset transfers.

Regulated entities verify sources of wealth to ensure that the net worth is accumulated through lawful activities. The entities verify the documents, such as tax returns, bank statements, will or testament documents, payslips, gift letters, inheritance documentation, etc., to check the source of wealth legitimacy.

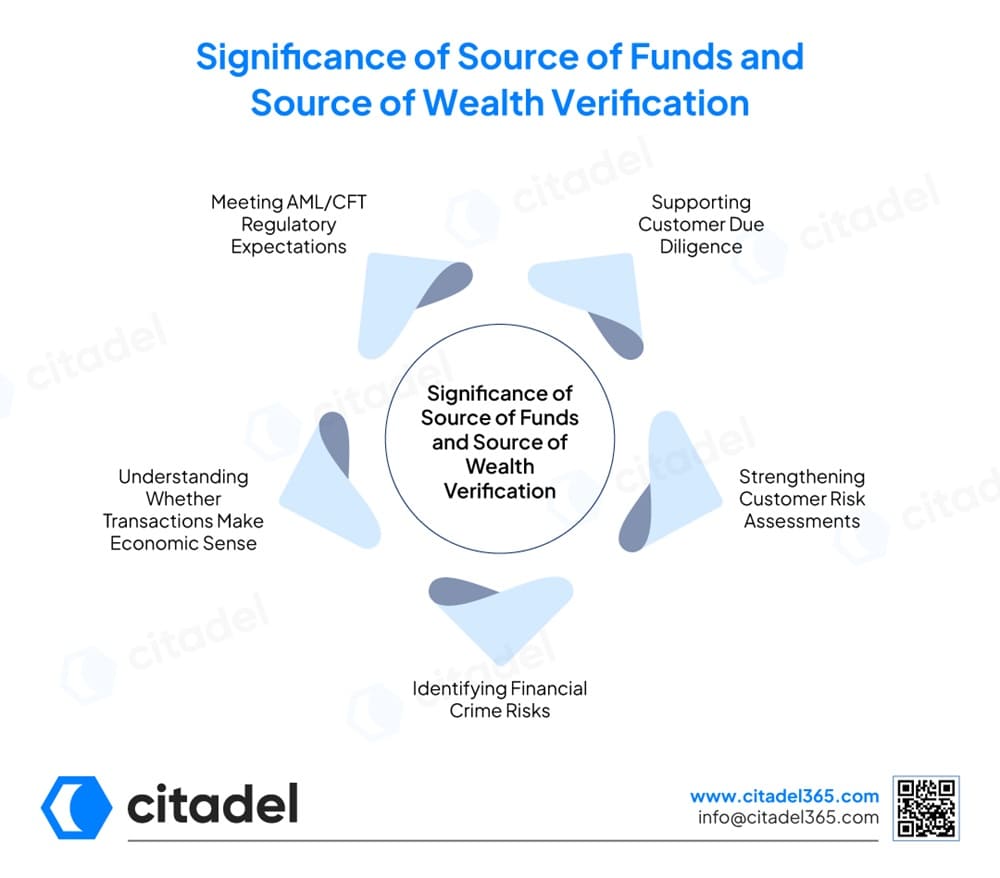

Regulated entities need to verify the sources of funds and wealth when conducting enhanced due diligence to ensure compliance with AML/CFT laws. Verifying SoF and SoW helps regulated entities in the UAE in the following ways:

Understanding SoF and SoW helps regulated entities get a clear picture of their customers. It allows verifying where the money comes from and understanding the overall financial background of the customer, thereby supporting customer due diligence.

SoF and SoW provide regulated entities with more detailed information about customers, helping validate the lawful origin of customers’ money. It further strengthens customer risk assessment by detecting anomalies and preventing ML/TF risks.

Verifying SoF and SoW helps uncover illicit proceeds by identifying structuring patterns, detecting corruption & bribery among PEPs, and preventing tax evasion and fraud by aligning customers’ activity with stated revenue.

SoF and SoW verification help determine the legitimacy of transactions. For instance, a large transaction that doesn’t match the customer’s profile is a red flag.

Regulators expect entities to assess SoF and SoW as part of their CDD obligations through applying a risk-based approach. Gathering SoF and SoW information helps regulated entities meet AML/CFT obligations.

Source of Funds and Source of Wealth checks are necessary when dealing with high-risk customers or processing large transactions. For high-risk customers such as politically exposed persons (PEPs), customers with complex ownership structures, or those linked to high-risk jurisdictions, these checks are necessary.

Further, during enhanced due diligence reviews and during large or unusual transactions such as luxury purchases, large deposits, or wire transfers, SoF and SoW checks are required.

Some of the common challenges when verifying the source of funds and the source of wealth include:

Regulated entities often make the following mistakes during SoF and SoW reviews:

Citadel365 provides a centralised platform for regulated entities in the UAE to consolidate customers’ financial information, customer data, and due diligence records, to simplify SoF and SoW reviews.

The software supports customer risk assessment and identifies high-risk customers for enhanced due diligence, which involves deeper verification of SoF and SoW. Further, Citadel365 helps regulated entities collect and manage documents, including bank statements, property documents, and other evidence for deeper scrutiny.

Citadel365 transaction monitoring software performs ongoing checks on high-risk customers, tracking customer transaction behaviours to support SoF and SoW reviews. Moreover, the case management software with effective audit trails supports record-keeping for compliance documents and helps regulated entities meet regulatory expectations.

Source of Funds focuses on a specific transaction and explains the origin of the funds in that transaction, while Source of Wealth helps explain a person’s accumulated wealth built over time.

Businesses ask for Source of Funds information to ensure the legitimacy of a transaction and understand whether it is not derived from illicit activities to combat ML/TF/PF risks.

Source of Wealth is important in AML compliance because it helps in understanding a customer’s financial background and establishing the legitimacy of their wealth.

Regulated entities should verify a customer’s source of funds when the customer is at high risk or engaged in high-value transactions or suspicious financial activities.

For customers at high risk, those involved with high-risk jurisdictions, or those engaged in unexpected complex transactions, the source of wealth should be verified.

Documents such as bank statements, tax returns, employment records, investment statements, inheritance documentation, property sale agreements, business ownership records, and financial statements help verify the source of funds.

Arjun is the Co-founder and CEO of Citadel, where he leads the company’s vision across technology, business, and regulations. He brings over a decade of experience in building and scaling technology ventures. Arjun holds a B.Tech. in Information Technology and a Master’s in Management, supported by his certification as a Financial Crime Specialist, an uncommon combination that allows him to balance innovation with regulatory requirements.

Having advised leading banks and financial institutions on digital solutions and compliance technology, Citadel continues to grow with an ambition.