Ready to Defeat Your AML Compliance Obstacles?

Citadel Brings Revolution with Secure Solutions to AML Compliance Problems

Customer Risk Assessment (CRA) software is an integral part of an organisation’s AML/CFT framework, helping it assess, classify, and monitor customer risk throughout the customer relationship. It is used by FIs, VASPs, and DNFBPs, including fintech companies, real estate firms, dealers in precious metals and stones, auditors, insurance providers, and other regulated entities throughout the UAE.

Customer risk assessment software automatically assesses customer profiles against various risk indicators, including customer type, geography, business activities, transactional behaviour, source of funds, source of wealth, and association with local or global sanctions watchlists. The software applies risk methodologies and scoring models to classify customer risk type as low, medium, or high-risk. It enables organisations to apply a risk-based approach (RBA) as required by the UAE AML/CFT regulations and international standards.

As AML/CFT regulations become more stringent, organisations face increasing challenges in conducting accurate and consistent customer risk assessments. Over-reliance on manual processes, fragmented data, and outdated systems often results in inefficiencies and heightens the compliance risk.

Some of the common challenges in customer risk assessment include:

Data Quality

Technological Disparity

Scaling Issues

Compliance Risks

Modern customer risk assessment (CRA) software helps with the automation of customer risk profiling, implementation of a risk-based approach, and enforcement of a greater degree of AML/CFT compliance.

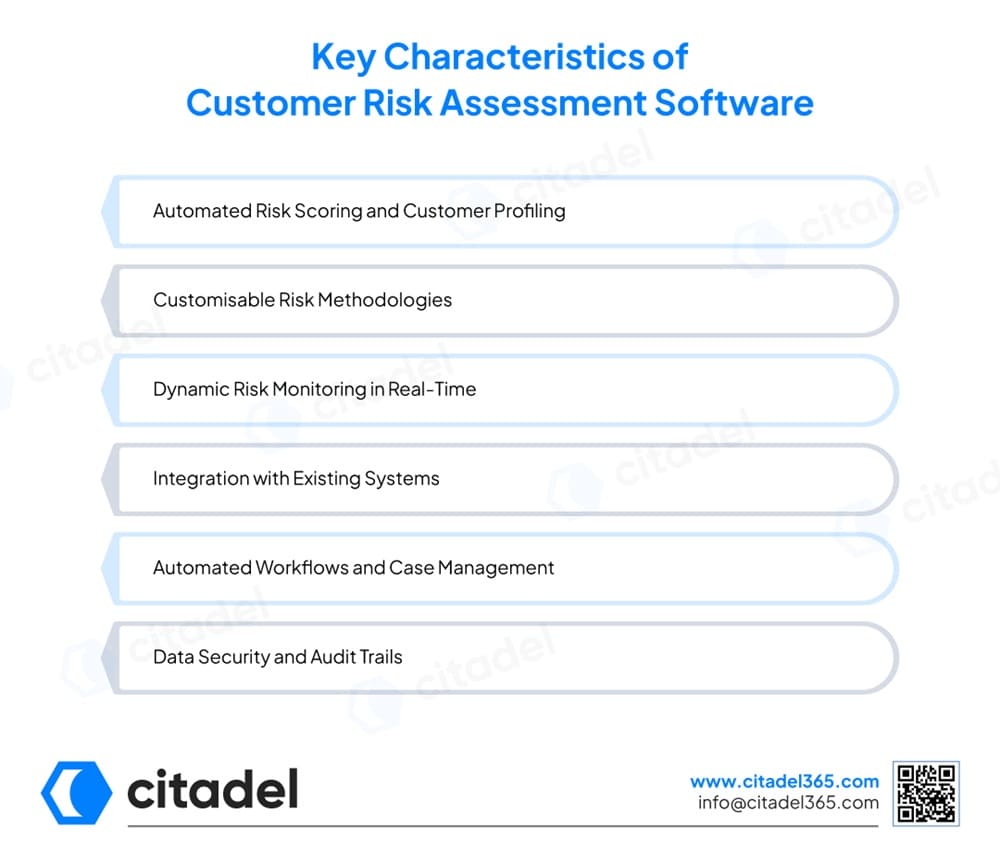

Some of the key features of Customer Risk Assessment Software include:

Automated Risk Scoring and Customer Profiling

Customer risk assessment software provides the automated assessment of customer risk based on a number of configurable risk elements such as customer type, geography, transaction behaviour, business activity, sanctions exposure, and adverse media findings. It assigns risk scores based on the assessment and classifies customers into low, medium, or high-risk categories.

Customisable Risk Methodologies

Customer risk assessment software enables organisations to customise their risk models, scoring logic, weightages, and assessment parameters in alignment with industry standards, risk appetite and regulatory requirements.

Dynamic Risk Monitoring in Real-Time

Risks associated with customers are dynamic. Risk assessment software helps in monitoring customer activities, behavioural patterns, sanctions updates, ownership structure, adverse media findings, and regulatory updates in real time. It also recalculates customer risk scores whenever there are any significant changes.

Integration with Existing Systems

Automated Workflows and Case Management

Risk assessment software automatically escalates and initiates appropriate compliance actions based on the classification of risk. This streamlined internal workflow helps compliance teams manage cases more efficiently and conduct Customer Due Diligence (CDD), Enhanced Due Diligence (EDD), approvals, escalations, and periodic reviews proportionate to the risk scores.

Data Security

Risk assessment software provides strong security controls to safeguard sensitive customer information, including role-based user access, data encryption, and activity logs.

By combining customer data, risk indicators, predefined scoring methodologies, and continuous monitoring capabilities, the risk assessment software helps regulated entities to implement an efficient and effective risk-based AML/CFT compliance framework.

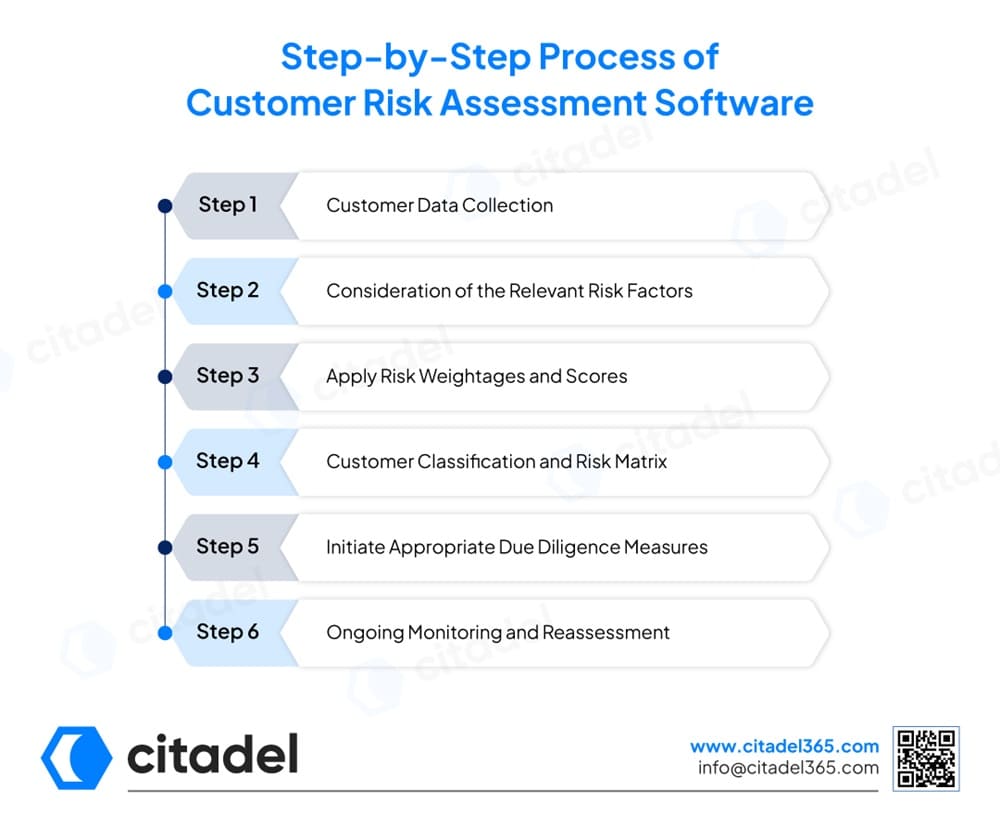

Here is how Customer Risk Assessment Software works:

The customer risk assessment software gathers critical customer information like identity details, source of funds and wealth, usual transactional behaviour, ownership structures, etc. This data is collected from various sources, such as onboarding forms, KYC documents, internal databases, APIs, and third-party systems.

The fragmented data is then verified and centralised into an actionable customer profile for risk assessment.

After data collection is complete, the AML risk assessment software analyses multiple risk factors associated with customer profiles. It considers the following risk categories of a customer relationship based on predefined risk parameters and compliance policies:

Customer risk assessment software then automatically assigns varying degrees of numerical importance (weightage) to each risk factor identified according to the organisation’s risk methodology. Using automated scoring models, the system calculates a composite customer risk score.

The generated risk score is then automatically plotted against a risk matrix by the software to categorise customers into predefined risk levels high, medium, or low. It generates a visual risk matrix often a colour-coded heatmap measuring likelihood and impact for a clear overview of customer risk exposure across the organisation.

Customer risk is ever evolving and keeps changing over time. The risk assessment software continuously monitors to detect unusual transaction behaviour, sanctions updates, profile information updates, ownership changes, etc. Whenever the thresholds are met, the software automatically recalculates the customer risk score, prompting manual reassessments or the escalation of appropriate due diligence measures.

Customer risk assessment (CRA) software does far more than simply assigning risk scores to customers. It helps in creating a stronger, faster, and more effective AML/CFT compliance framework by automating risk evaluation methodologies, which enable proactive risk assessments and management.

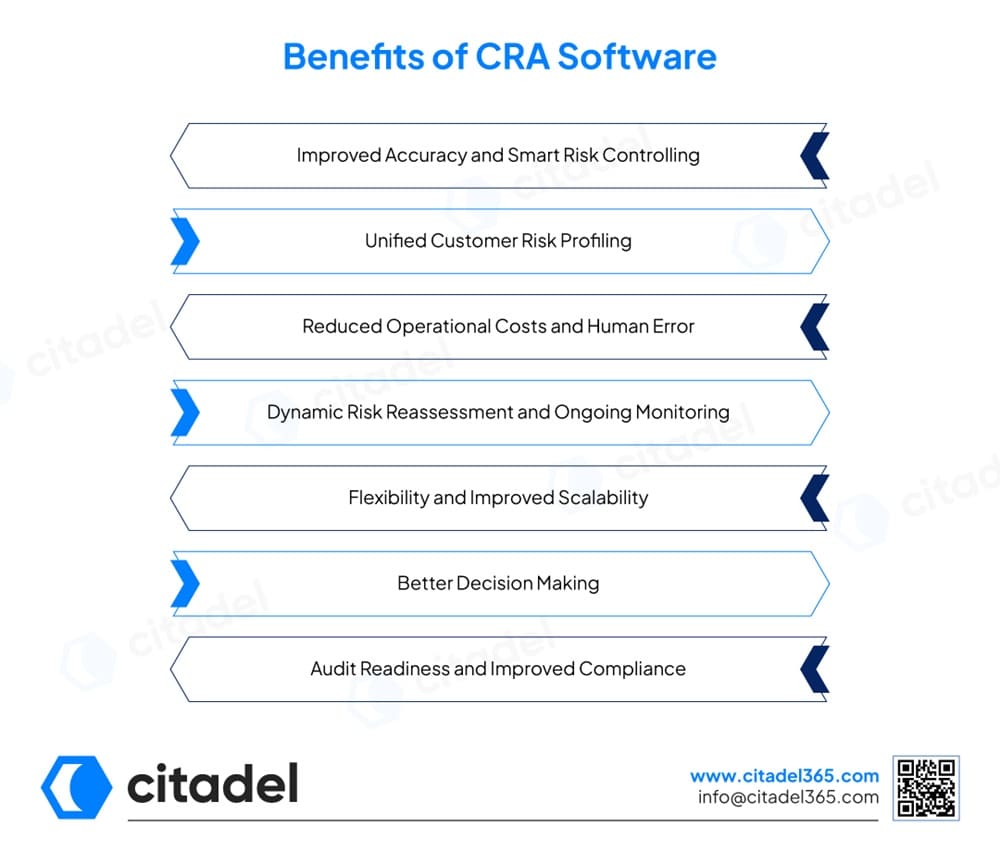

Some of the key benefits of customer risk assessment (CRA) software are:

Improved Accuracy and Smart Risk Controlling

Risk assessment software helps REs to assess customer risks using intelligent and automated risk evaluation models to go beyond basic verification. It helps detect and analyse risk indicators such as customer behaviour, transaction patterns, geographic exposure, business activities, sanctions associations, and adverse media findings. This improves risk identification accuracy and enables organisations to apply appropriate risk-based controls.

Unified Customer Risk Profiling

Customer risk assessment software has the ability to integrate customer information, KYC records, screening results, transaction behaviour, and diverse risk indicators into a centralised customer risk profile. This centralised view enables organisations to:

Reduced Operational Costs and Human Error

AML risk assessment software reduces dependency on slow manual processes, eliminating repetitive tasks, inconsistency, and human errors. It automates calculations, workflows, and monitoring activities and cuts down operational costs while also reducing oversight risks, enabling staff to focus on high-risk customers. It also reduces onboarding delays and improves operational efficiency.

Dynamic Risk Reassessment and Ongoing Monitoring

Customer risk evolves continuously. CRA software monitors changes in ownership, transaction behaviour, sanctions exposure, and adverse media, and automatically recalculates risk scores keeping profiles current throughout the customer lifecycle.

Flexibility and Improved Scalability

An effective risk assessment software is highly configurable and adaptable according to the latest regulatory requirements, increasing customer volume and changing business models. It can be customised as per the specific needs of a particular industry. As businesses grow, this flexibility enables them to maintain a robust and scalable AML/CFT compliance framework.

Better Decision Making

Audit Readiness and Improved Compliance

CRA software maintains complete audit trails and risk records, making it straightforward to demonstrate compliance during inspections and regulatory reviews.

By automating risk evaluation, customer profiling, classification, monitoring, and documentation, the customer risk assessment software helps identify high-risk customers and apply proportionate controls to comply with UAE regulatory requirements.

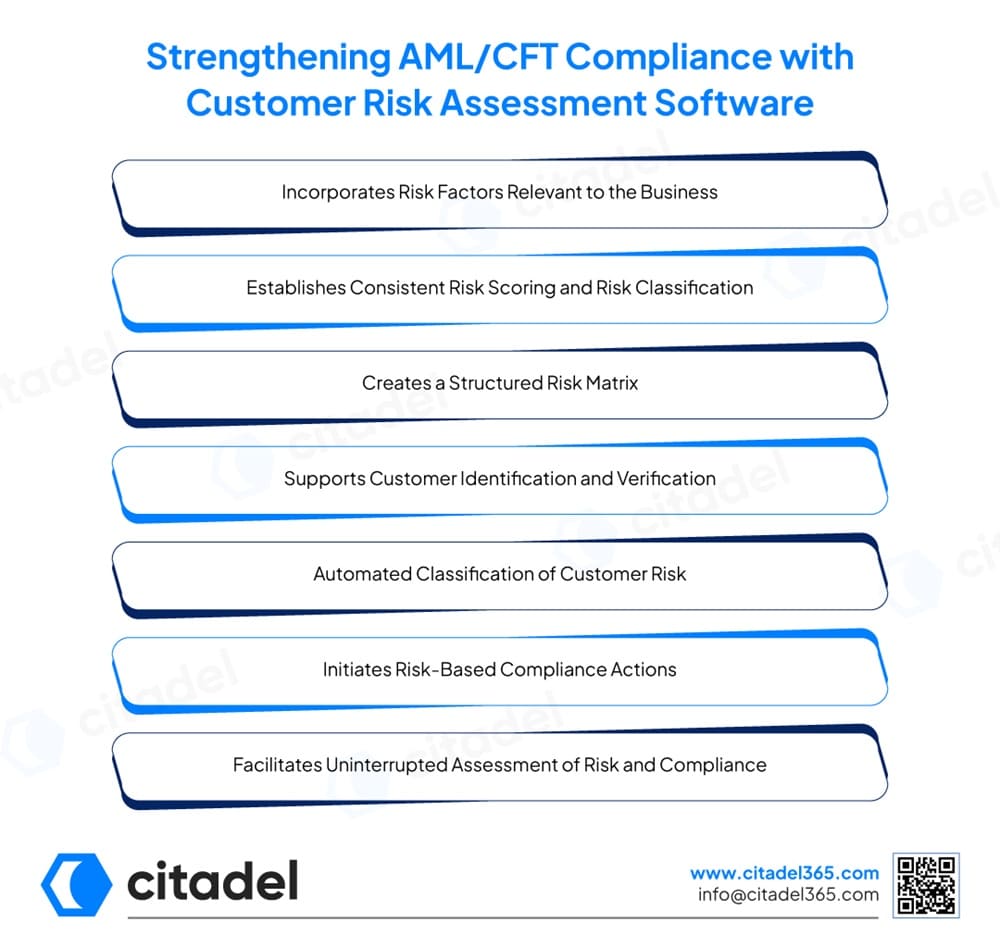

Incorporates Risk Factors Relevant to the Business

Every organisation has a different set of challenges when it comes to the nature of its business. Customer risk assessment software with flexible risk factor configuration enables organisations to set risk factors in line with their risk appetite, the structure of the applicable laws, and the internal compliance policies.

Risks associated with the following can be evaluated using the risk assessment software:

Establishes Consistent Risk Scoring and Risk Classification

Customer risk assessment software utilises a defined scoring system and risk weightage to provide an assessment of ML, TF, and PF risks. The significance of each risk factor is considered, and the software computes customer risk scores.

This uniformity helps organisations:

Creates a Structured Risk Matrix

The software provides a risk matrix that is fully configurable and structured to map weighted risk factors, risk levels, and customer scoring. This structure aids the compliance team in providing a pictorial and transparent means of determining customer risk ratings.

The matrix can be tailored to fit the organisation’s policies and the risk landscape.

Supports Customer Identification and Verification

Risk assessment software integrates with KYC, Customer Onboarding, CRM, and Document Management Systems to collect and process customer information automatically.

The software can evaluate information derived from various documents:

For Individual Customers

Document | Key Information Extracted For CRA | How It Helps |

Emirates ID / Passport / Driving License | Name, nationality, date of birth, issuance and expiry dates of documents.

| Help identify customer-specific risks, geographic exposure, and any connection with high-risk jurisdictions to enable application of risk-based measures. |

Utility Bill / Municipal Tax Record / Rent Agreement | Residential address information used to identify customer location and assess geographic risk exposure. | Helps determine whether the customer is connected to sanctioned or higher-risk jurisdictions requiring additional due diligence measures. |

Bank Statement | Customer’s financial standing, account activity, transaction behaviour, and geographic exposure. | Helps identify transaction-related risks, unusual financial patterns and behaviour, and potential reporting obligations such as SARs or STRs. |

For Corporate Customers

Document | Key Information Extracted for CRA | How it Helps |

Trade Licence / Memorandum of Association (MOA) / Articles of Association (AOA) / Certificate of Good Standing / Certificate of Incorporation | Business registration details, legal status, ownership information, nature of business, and legitimacy of operations. | Help assess customer-specific risks, business risks, geographic exposure, and identify potential shell companies. |

Utility Bill / Municipal Tax Records / Property Documents / Rent Agreement / Insurance Policy | Registered business address and proof of operational presence. | This information is used to assess geographic risk and identify false, non-operational, or dummy business addresses. |

Bank Statement | Financial standing, transaction activity, geographic exposure, cross-border transactions, and potential virtual asset-related activities. | Helps assess unusual transaction behaviour and related jurisdictional risks. |

Audited Financial Statements | Financial health, business performance, revenue sources, and overall financial standing of the entity. | These insights help evaluate the customer’s financial legitimacy and potential risk exposure. |

Register of Shareholders / Register of Directors / UBO Declaration/ Board Resolution Appointing Authorised Signatory

| Ownership structure, Ultimate Beneficial Owners (UBOs), controlling persons, directors, and authorised representatives. | This information is critical for assessing ownership transparency and identifying hidden ownership risks. |

This aids in determining customer information validity and improves the accuracy of the customer’s risk assessment.

Automated Classification of Customer Risk

Upon evaluating the customer’s data and risk indicators, the software classifies customers into risk categories.

Automated classification enables the entity to:

Automatically Computes Customer Risk Score

The customer risk assessment software automatically computes the customer risk score based on the risk factors and their assigned weights. This allows the entity to assess customer risk in a more objective and systematic manner, rather than through qualitative assessments alone.

Initiates Risk-Based Compliance Actions

A significant advantage of the CRA software from an AML/CFT perspective is the software’s ability to automatically implement requisite compliance actions based on customer risk ratings.

For example, the software will implement:

This ensures that necessary compliance actions are undertaken proportionate to the estimated risk.

Facilitates Uninterrupted Assessment of Risk and Compliance

Customer risk profiles are subject to change based on the customer’s behaviour, ownership changes, sanction applicability, adverse media, and other regulatory changes. The customer risk assessment software assesses these factors dynamically, and customer risk profiles are adjusted accordingly, keeping them current and relevant throughout the duration of the relationship.

Keeps Proper Record of Risk Methodology

Regulators want to see how organisations assess and manage risks associated with their customers. Customer risk assessment software records the following:

This increases transparency and helps with a regulatory review and internal audit.

Maintains an Audit Trail

For building a robust and effective risk-based AML/CFT compliance framework, it is imperative for REs to choose the right customer risk assessment (CRA) software.

Some of the must-have features are the following:

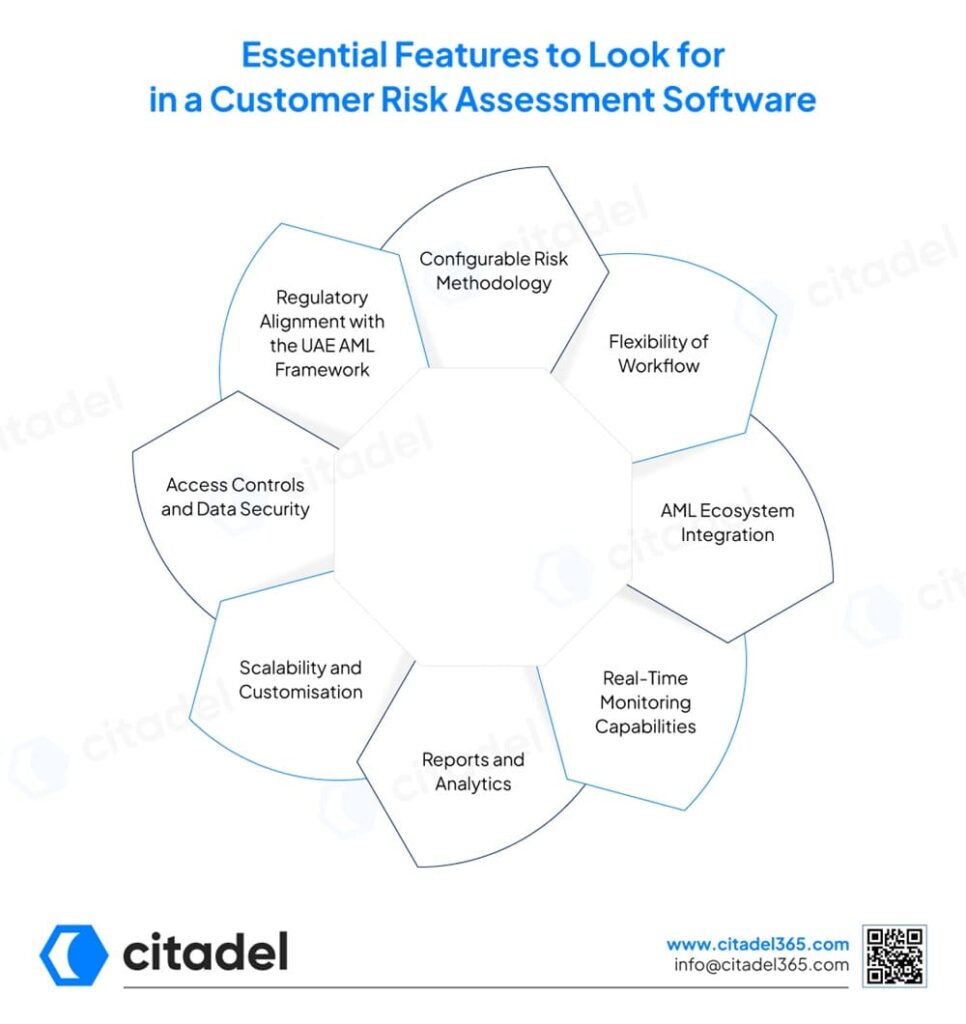

1. Configurable Risk Methodology

Every organisation has a specific business model with a unique risk profile. An effective CRA system would allow configuration of risk factors, scoring methodologies, weightages, and risk thresholds based on the specific industry standards, the business’s risk appetite and compliance requirements.

2. Flexibility of Workflow

Customer risk assessment software should have flexible workflows that align with the organisation’s internal governance controls. It should automate and support customisable workflows to ensure seamless user handling.

3. AML Ecosystem Integration

An effective CRA solution should integrate smoothly with other compliance systems like KYC and customer onboarding platforms, sanction and PEP screening solutions, transaction monitoring systems, etc. This minimises friction across the system and improves efficiency, data consistency, and overall risk visibility.

4. Real-Time Monitoring Capabilities

Customer risks are never static; they evolve and require continuous real-time assessment. A CRA system must have the capability to conduct ongoing monitoring of customer activities, sanctions updates, ownership changes, adverse media findings, and other risk indicators to ensure risk scores and profiles are immediately updated and remain accurate.

5. Reports and Analytics

A customer risk assessment software must have an automated and comprehensive dashboard along with detailed reporting abilities to enhance visibility into customer risk exposure, high-risk relationships, review status, and regulatory changes. This supports internal audits, management oversight, and external reviews.

6. Scalability and Customisation

Customer risk assessment software must be capable of adapting to increasing customer volumes as businesses expand. Scalability is important to ensure compliance effectiveness while adapting to organisational growth and changing risk environments.

7. Access Controls and Data Security

Risk assessment software must have robust security controls as it handles sensitive customer information. It must have role-based access permissions, user authentication, data encryption, activity logs, and secure data storage to protect confidential customer data.

8. Regulatory Alignment with the UAE AML Framework

Organisations are required to implement a risk-based approach and comply with applicable UAE AML/CFT regulations. The customer risk assessment software must be able to support guidance issued by supervisory authorities and industry best practices.

The future of Customer Risk Assessment (CRA) in the UAE is rapidly shifting from traditional, time-based, reactive reviews to smart, proactive, continuous, risk-based compliance models. As the UAE strengthens its AML/CFT framework ahead of increasing regulatory scrutiny and the FATF Fifth-Round Mutual Evaluation, regulators are placing greater emphasis on demonstrating compliance effectiveness rather than simply maintaining documented policies.

Traditional customer risk assessments are often conducted during onboarding and periodic reviews. However, future CRA frameworks will focus on continuous monitoring, dynamic risk profiling, and real-time reassessment of customer risks based on behavioural changes, transaction activity, sanctions exposure, adverse media findings, and evolving financial crime threats.

AI-Driven Risk Assessment and Decision-Making

The role of customer assessment in the risk management lifecycle will be greatly enhanced by AI and ML, as these systems will assist businesses more effectively in identifying hidden risk patterns, prioritising high-risk relationships, reducing false positives, and improving the accuracy of customer risk scoring. However, regulatory expectations will continue to require strong governance, transparency, and human oversight over AI-driven compliance decisions.

Stronger Emphasis on Risk-Based Compliance

The UAE regulatory landscape is increasingly moving towards a demonstrable risk-based approach in which businesses are required to articulate how customer risk is identified and assessed, and the measures employed to actively monitor and control it. Compliance frameworks will be expected to allocate resources proportionately to higher-risk customers, products, services, and jurisdictions, while maintaining clear documentation of risk methodologies and decision-making processes.

Better Integration Across AML Ecosystems

The next generation of CRA solutions will be part of a connected compliance ecosystem, integrating customer onboarding, KYC, sanctions screening, adverse media monitoring, transaction monitoring, and case management systems. This unified approach will allow organisations to gain a comprehensive and real-time view of customer risk exposure.

Greater Attention to New and Emerging Risks and Proliferation Financing

Technology-Based Compliance Will Become the Standard

With the changing customer, financial crime, and regulatory compliance landscapes, technology-based CRA solutions will be critical for the UAE to meet continuous regulatory compliance pertaining to AML/CFT, and manual customer risk assessment processes will become increasingly unsustainable. Technology-driven customer risk assessment solutions that combine automation, advanced analytics, real-time monitoring, and adaptive risk scoring will become the norm.

Citadel365 makes automating customer risk scoring, due diligence workflows, and the continual monitoring of customer risk easier with its Customer Risk Assessment (CRA) solution. Organisations using the Citadel365 platform can evaluate customers to determine risk levels based on customer profile, geography, transaction behaviour, sanctions exposure, PEP status, and adverse media.

With configurable risk methodologies, automated customer classification, and continuous risk reassessment, Citadel365 helps businesses identify high-risk customers quickly and apply appropriate AML/CFT controls. The platform also provides an automated and seamless integration to KYC, customer onboarding, sanctions screening, and all other AML compliance systems to create a unified compliance ecosystem. By combining automation, flexibility, and real-time risk intelligence, Citadel365 helps organisations strengthen AML/CFT compliance, improve operational efficiency, and implement a more effective risk-based approach.

Several risk factors are considered during customer risk assessment, including customer type, business activities, location, products and services used, transaction behaviour, source of funds/wealth, delivery channels, sanctions or PEP exposure, and adverse media links.

A risk-based approach aims to apply proportionate controls to ML/TF/PF risks, as resources are always scarce. Customers posing higher risks are subject to stronger controls to keep ML/TF/PF risks at a manageable level.

Customer risk assessments should be reviewed and updated on a periodic basis according to the customer’s risk profile. It should be triggered in the event of material changes to the ownership structure, business activities, transaction behaviour, geographic exposure, and changes in the applicable regulations.

Yes, customer risk assessment software integrates with various AML systems, including KYC platforms, customer onboarding systems, sanctions and PEP screening tools, adverse media monitoring platforms, transaction monitoring systems, case management tools, etc., to create a centralised AML/CFT compliance framework.

Challenges that businesses face with customer risk assessment processes include obtaining accurate customer information, maintaining consistent risk scoring, managing large customer volumes, conducting real-time assessments, and keeping pace with fast-changing regulations.

Automated risk scoring eliminates manual calculations and applies predefined risk methodologies consistently across all customer profiles. Applying consistent risk scoring methods across all customer accounts improves accuracy and reduces the likelihood of scoring errors. It speeds up customer onboarding and allows compliance teams to concentrate on higher-risk accounts and investigations.

Customer risk is very dynamic and can change over time. Continuous monitoring can help organisations rapidly respond to shifting risks by identifying changes in transaction behaviour, ownership structure, sanctions exposure, adverse media findings, or emerging financial crime threats, and implement appropriate compliance responses.

Some red flags include high-risk jurisdictions, complex ownership structures, unusual transaction behaviour, large cash-intensive activities, sanctions or PEP associations, negative media connections, unexplained sources of funds or wealth, and frequent changes in business or account activity.

Arjun is the Co-founder and CEO of Citadel, where he leads the company’s vision across technology, business, and regulations. He brings over a decade of experience in building and scaling technology ventures. Arjun holds a B.Tech. in Information Technology and a Master’s in Management, supported by his certification as a Financial Crime Specialist, an uncommon combination that allows him to balance innovation with regulatory requirements.

Having advised leading banks and financial institutions on digital solutions and compliance technology, Citadel continues to grow with an ambition.