Ready to Defeat Your AML Compliance Obstacles?

Citadel Brings Revolution with Secure Solutions to AML Compliance Problems

Customer Due Diligence (CDD) is a process that involves collecting customer information, verifying their identities, assessing their risk profiles, and monitoring them continuously to prevent money laundering, terrorist financing and other financial crimes. In the UAE, it is mandatory for DNFBPs, including real estate agents and brokers, to implement CDD into their daily operations.

Real estate agents and brokers must apply CDD measures upon the commencement of a business relationship, when they suspect criminal activity, and when existing customer information is incomplete, inaccurate, or outdated, as stated in Federal Decree Law No. 10 of 2025.

The Ministry of Economy and Tourism (MoET) is the supervisory body for real estate agents and brokers in the UAE. Under Cabinet Resolution 134 of 2025, real estate agents and brokers must conduct risk-based CDD, identify & verify the beneficial owner, apply enhanced due diligence and perform ongoing monitoring to combat ML/TF risks.

Real estate agents and brokers must conduct customer due diligence on all parties who are involved in the property transaction. Regulated entities must identify and verify the following:

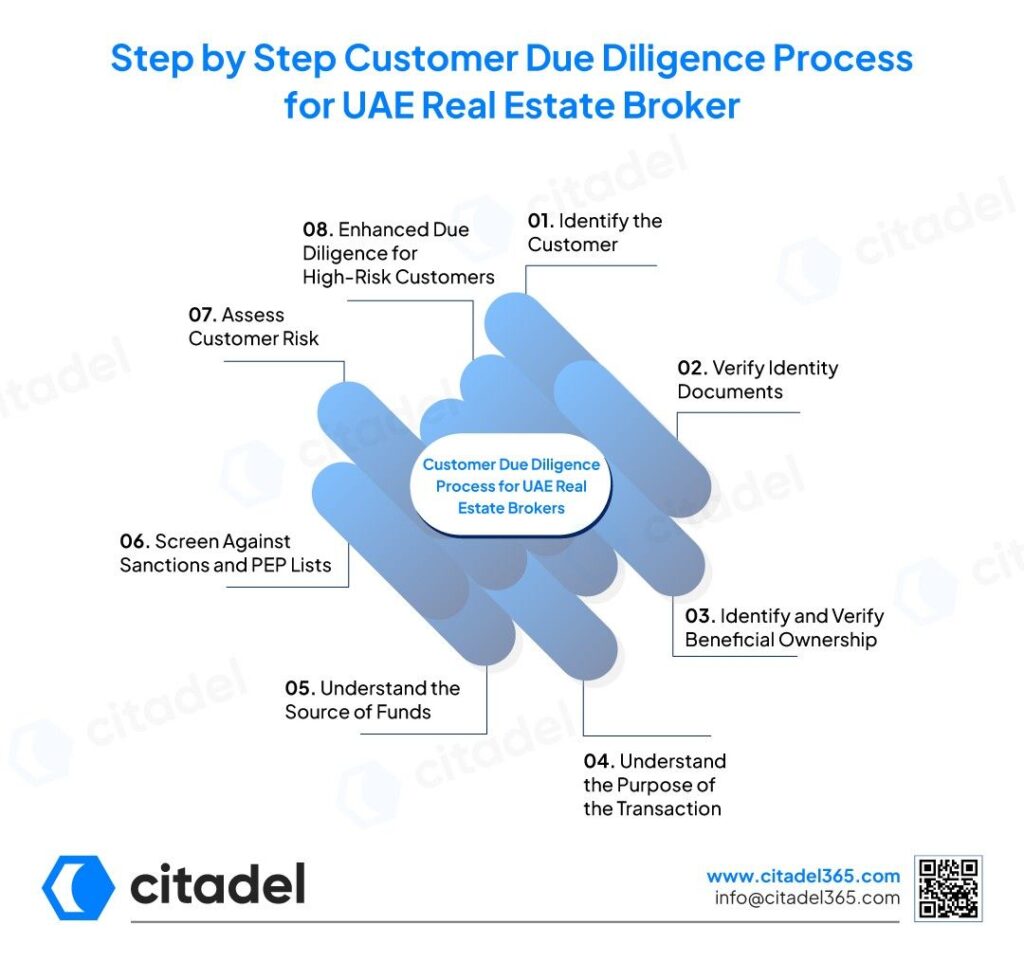

Real estate brokers and agents in the UAE must follow a comprehensive CDD process, which involves customer & UBO identification & verification, risk assessment, screening, and enhanced due diligence. The following points make the CDD process clearer:

Collect basic customer information, including their name, address, contact details and legal status.

Verify customer identity using reliable documents such as a passport, Emirates ID, trade license, or any other valid government-issued identity document.

Brokers must identify and verify beneficial owners, or persons who ultimately own or control the corporate business (holding 25% or more shares/voting rights), when dealing with a legal-entity customer.

Real estate agents and brokers must examine the customer’s purpose of buying, selling or investing in a property and whether it aligns with the customer’s stated profile.

Real estate brokers and agents must evaluate the origin of money used in the property transaction and ensure the legitimacy of funds.

Screen customers, beneficial owners, or any parties involved in property transactions against the sanctions lists and politically exposed person (PEP) databases to determine high-risk customers.

Brokers must assess customer risk based on factors such as customer type, transaction value, geographic exposure, etc.

When a customer is identified as high-risk, such as PEP, or engages in complex transactions, real estate brokers and agents should conduct enhanced due diligence, including deeper background checks and increased ongoing monitoring.

Real Estate Brokers must collect the relevant information to identify and verify customers during CDD and to comply with the AML/CFT regulations in the UAE. The basic information for CDD includes the following:

Individual Customer Information

Corporate Customer Information

Transaction-Related Information

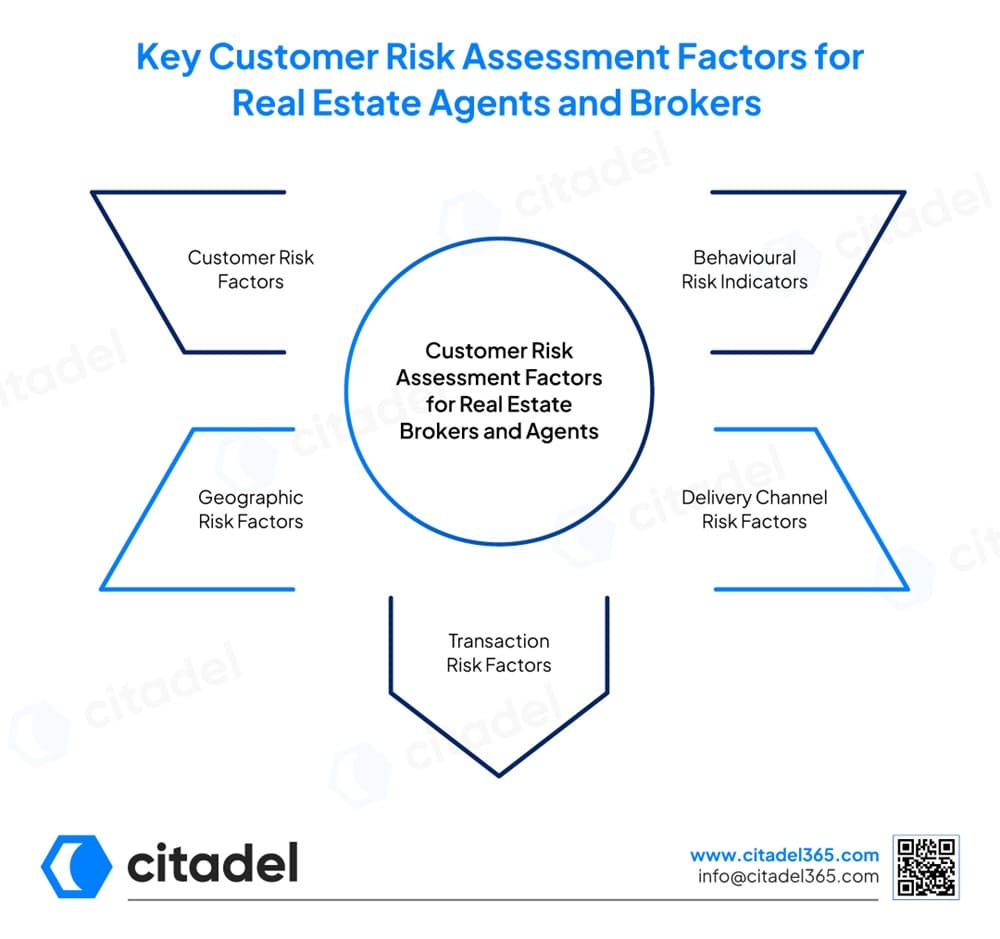

Real estate brokers and agents assess customer risk through evaluating the following factors:

Customer Risk Factors

Evaluate the customer’s background, business activity, occupation, ownership structure, and PEP status.

Geographic Risk Factors

Identify nationality, country of residence, and business operations in/with high-risk jurisdictions.

Transaction Risk Factors

Assess the nature of the transaction, mode of payment, transaction value, and whether they match the customer’s stated profile. Check frequent property transfers, high-value property purchase/sale, third-party payments, and the source of funds associated with a transaction.

Delivery Channel Risk Factors

Assess transactions involving intermediaries, agents, and non-face-to-face interactions.

Behavioural Risk Indicators

Evaluate whether the customer’s behaviour poses a risk, such as unusual urgency, inconsistent documentation, or reluctance to provide information.

While customer due diligence is a standard AML obligation during the onboarding process to identify & verify customers, enhanced due diligence is necessary for high-risk customers. It involves a deeper investigation, requiring a source of wealth check and increased ongoing monitoring. Real estate agents and brokers must apply enhanced due diligence in the following cases:

Real estate brokers in the UAE must constantly watch for or identify the following red flags or warning signs to combat ML/TF risks:

Customer Due Diligence is an ongoing process with ongoing due diligence as an essential component. Real estate agents and brokers are required to continuously monitor customers, transactions, and business relationships after customer onboarding. This involves:

Recordkeeping is an essential requirement under Cabinet Resolution No. 134 of 2025, requiring real estate brokers and agents to keep records for at least 5 years. Real estate brokers and agents are required to maintain records of customer identification documents, transaction data, beneficial ownership information, CDD processes, source of funds information, and suspicious activity reviews.

Recordkeeping is necessary for real estate agents and brokers to be made available when requested by regulatory authorities. This serves as evidence of compliance with AML/CFT obligations and supports brokers and agents from regulatory penalties and compliance risks.

Real estate brokers and agents face the following challenges while conducting CDD:

Citadel365 accelerates the customer due diligence process with multi-channel data capture that replaces slow and manual onboarding and streamlines customer information collection. Further, it automates customer risk assessment by helping calculate risks at onboarding and profile risk, providing a weighted risk score.

Its name screening software screens customers against PEP databases and sanctions lists to identify high-risk customers and apply required procedures. Further, Customer Onboarding Software provides ongoing monitoring functionality of the customer information and transactions.

Moreover, Citadel365 ensures audit-ready customer records with immutable timestamped audit trails and a centralised platform for compliance operations. Therefore, it helps UAE real estate agents and brokers to meet regulatory requirements with ease, eliminating human errors, transaction delays, and manual paperwork.

UAE real estate brokers are required to conduct CDD before establishing a business transaction, while carrying out an occasional transaction, and when there is a suspicion of ML/TF activity.

Real estate agents and brokers should collect identification documents and transaction-related information for both individual and legal entity customers.

Yes, real estate brokers are required to identify and verify beneficial owners to comply with regulatory requirements and prevent concealment of illicitly obtained funds.

CDD is an effective AML control applied to all customers, which includes identifying and verifying customers’ information, assessing risk and monitoring them. EDD includes a deeper investigation of high-risk customers, requiring checks of the source of funds and wealth, and increased monitoring.

In the UAE real estate sector, a customer is classified as high risk when their profile, transaction patterns, or source of wealth indicate elevated risks for money laundering or other financial crime. Real estate brokers and agents must conduct enhanced due diligence for clients, including PEPs, and for customers from high-risk jurisdictions.

Arjun is the Co-founder and CEO of Citadel, where he leads the company’s vision across technology, business, and regulations. He brings over a decade of experience in building and scaling technology ventures. Arjun holds a B.Tech. in Information Technology and a Master’s in Management, supported by his certification as a Financial Crime Specialist, an uncommon combination that allows him to balance innovation with regulatory requirements.

Having advised leading banks and financial institutions on digital solutions and compliance technology, Citadel continues to grow with an ambition.