Ready to Defeat Your AML Compliance Obstacles?

Citadel Brings Revolution with Secure Solutions to AML Compliance Problems

Financial institutions and Designated Non-Financial Businesses and Professions (DNFBPs) operating in the UAE, as a part of complying with AML regulations, are expected to apply a risk-based approach in their AML/CFT frameworks. The aim of the RBA is to identify customers who present a higher risk of money laundering, terrorist financing, or other financial crimes.

Understanding what makes a customer high risk is critical for applying the appropriate level of due diligence, ensuring regulatory compliance, and protecting businesses from financial and reputational risk.

This article explains how UAE AML regulations define customer risk, the characteristics of high-risk customers, and how technology can help organisations strengthen customer risk assessments.

Under the UAE’s Anti-Money Laundering framework, Financial Institutions and Designated Non-Financial Businesses and Professions (DNFBPs) are required to apply a risk-based approach to identify, assess and manage customer risks. The same level of scrutiny cannot be applied to every customer, but should be proportionate to the customer’s risk profile, after assessing the potential money laundering, terrorist financing and proliferation financing risks arising from each customer relationship.

The risk assessment of a customer will determine the level of due diligence required and whether the customer needs to be subject to ongoing scrutiny and monitoring.

Customer risk assessment is a tool used by organisations to assess the risk of financial crime posed by an individual customer. By assessing factors such as customer identity, business activities, geographic exposure, ownership structures and transaction behaviour, businesses can identify customers who may pose a higher risk of money laundering or terrorist financing.

The functions of the customer risk assessment process are:

A sound customer risk assessment process helps organisations make informed decisions, remain compliant with regulations, and protect their business from potential exposure to illicit activity.

The UAE implements a Risk-Based Approach (RBA) to AML compliance in accordance with the recommendations issued by the Financial Action Task Force (FATF). This technique involves the assessment of the particular risks posed by individual customers and their subsequent categorisation.

Customers are normally categorised into risk levels such as:

The level of due diligence and monitoring required is determined by classification.

Customer risk ratings are determined using a number of risk indicators, not simply one factor. As per UAE AML laws, companies need to screen customers against a wide variety of risk factors.

Factors that commonly affect risk ratings include:

Each factor contributes to the total risk profile to help organisations determine if a customer is low, medium or high risk.

Customer risk assessments should never be a one-off exercise for onboarding purposes only. Customer circumstances can change over time, which may affect their associated risks.

Events that could lead to a reassessment of customer risk include:

Ongoing monitoring and periodic reviews also ensure that customer risk ratings are accurate and up to date throughout the customer life cycle. This ongoing process helps organisations to identify emerging risks early, apply the right controls and remain in compliance with UAE AML regulations.

In the UAE, AML regulations define a high-risk customer as one whose profile and activities, ownership structure, geographic exposure or transaction behaviour suggest a higher likelihood of money laundering, terrorist financing or other financial crimes. High-risk customers need enhanced due diligence (EDD) where required, increased monitoring, and more frequent risk reviews to comply with the regulations.

While no single factor will automatically decide a customer’s risk level, the presence of one or more risk indicators can significantly increase the overall risk rating.

Politically Exposed Persons (PEPs)

Politically Exposed Persons (PEPs) are persons who are or have been entrusted with prominent public functions, such as heads of state or government, senior politicians, judges, military officers, and senior executives of government-owned corporations.

With regard to foreign PEPs and domestic PEPs identified as high-risk, regulated entities are required to apply Enhanced Due Diligence (EDD) measures and appropriate ongoing monitoring for business relationships.

Customers Connected to High-Risk Jurisdictions

Higher risk is often associated with customers linked to countries with weak AML controls, high corruption, terrorist-financing concerns or sanctions exposure. Geographic exposure may arise through residency, citizenship, business operations, ownership structures, or transactional activity.

Businesses have to carry out due diligence on customers associated with jurisdictions that have been listed as high in AML risks by international organisations such as the Financial Action Task Force (FATF).

Customers with Complex Ownership Structures

Corporate structures can be complex and difficult to understand, making it difficult to determine who owns or controls a business. The real ownership can be hidden behind layers of companies, offshore entities, trusts, holding companies or cross-border ownership arrangements.

While complex structures are not necessarily illegal, they may increase AML risk as they can offer opportunities to conceal illicit funds or beneficial ownership.

Customers with Unclear Beneficial Ownership

One of the biggest AML risk factors is the inability to identify the ultimate beneficial owner of a customer. Where ownership information is incomplete, inconsistent, or deliberately obscured, organisations may find it difficult to determine who has ultimate control over the entity.

Customers who decline or are unable to provide ownership transparency often face increased scrutiny and may be considered high risk.

Customers with Unexplained Sources of Funds or Wealth

Where required, customers should be able to show where they got the money used for transactions or explain how they accumulated their wealth in the first place. There is a substantially increased risk of money laundering when customers are unable or refuse to provide adequate explanations or supporting documentation for the source of their funds.

Organisations may need to seek further evidence, such as financial records, tax documents, contracts or asset ownership information, to confirm the legitimacy of funds.

Cash-Intensive Businesses and Industries

Businesses that deal a lot in cash are potentially considered to be higher risk, because cash transactions are harder to track and verify. The reason is that these industries depend on cash payments that are not always transparent.

For example:

The level of risk depends on the nature, size and geographical exposure of the business.

Customers Conducting Unusual or Complex Transactions

Customer risk assessment is heavily dependent on transaction behaviour. Transactions that are unusually large, unnecessarily complex or inconsistent with known business activities may require additional scrutiny.

For instance:

Such activities may represent attempts to conceal the source, destination or ownership of funds.

Non-Resident Customers with Limited Economic Presence

Non-resident customers with limited business activities, physical presence, or economic connections to the jurisdiction in which they conduct transactions may pose additional risks.

For example, A company formed in one country, doing its principal business remotely and with no apparent commercial reason for doing so, may require enhanced due diligence to confirm the purpose of the relationship and confirm its legitimacy.

Customers Associated with Adverse Media or Criminal Allegations

Adverse media screening can uncover negative information that could have a significant impact on a customer’s risk profile.

While adverse media doesn’t necessarily mean there is any wrongdoing, it is an important risk indicator that should be researched and captured during the customer risk assessment process.

Customers Using Third Parties, Nominees, or Intermediaries

The involvement of third parties, nominees, agents or intermediaries can make it difficult to identify the true beneficiaries of a transaction or business relationship. Such arrangements may be legitimate in some cases; however, they can also be used to obscure ownership, control or the actual purpose of financial activities.

Organisations should carefully assess such relationships, verify the identity of all parties involved and ensure transparency regarding beneficial ownership and true control before classifying the customer’s final risk level or score.

One of the most scrutinised customer categories worldwide, including in the UAE, under AML regulations, is Politically Exposed Persons (PEPs). Because of the positions they hold or have previously held, increased controls are anticipated for businesses when setting up and maintaining relationships with these individuals.

But it is important to know that PEP status does not automatically indicate criminal activity. Instead, it implies an increased level of potential risk that requires additional due diligence and ongoing monitoring.

Who Qualifies as a PEP?

A Politically Exposed Person is always a natural person who is or has been entrusted with a prominent public function and has influence over the spending of government funds. PEPs generally have three broad categories:

Depending on the jurisdiction and regulatory framework, PEPs include:

Organisations need to have effective screening procedures to identify customers falling within these categories at both the onboarding stage and throughout the customer relationship.

Why PEPs Present Elevated AML Risks

PEPs are considered higher-risk customers whose positions may create opportunities to influence public decisions, control government resources or access significant public funds. This influence can create exposure to certain risks, such as:

In the UAE, businesses are required to apply Enhanced Due Diligence (EDD) measures when dealing with PEPs. These measures help organisations better understand the customer’s source of wealth, source of funds, and overall risk profile.

Family Members and Close Associates of PEPs

AML obligations often go beyond the PEPs themselves. Family members and close associates can also elevate AML risks, as they can be used to hide assets, transfer funds or conduct transactions on behalf of the PEP.

Because of these close and interlinked connections, businesses are required to assess not only the PEPs but also related individuals and entities that may be linked to them.

Do All PEPs Automatically Become High Risk?

No, not all PEPs are necessarily high risk. The status of a PEP is a major risk factor, but in the UAE, organisations are encouraged to adopt a risk-based approach rather than applying a blanket classification to all PEPs.

Additional factors that should be considered in the ultimate risk rating include:

In practice, many organisations treat PEPs as high risk due to regulatory expectations and the additional due diligence requirements that come with such relationships. However, risk assessments should be proportionate, documented and based on the customer’s overall risk profile and not just PEP status.

A robust AML program should combine PEP screening, risk scoring, enhanced due diligence, and ongoing monitoring to ensure that politically exposed customers are managed effectively in adherence with UAE regulations.

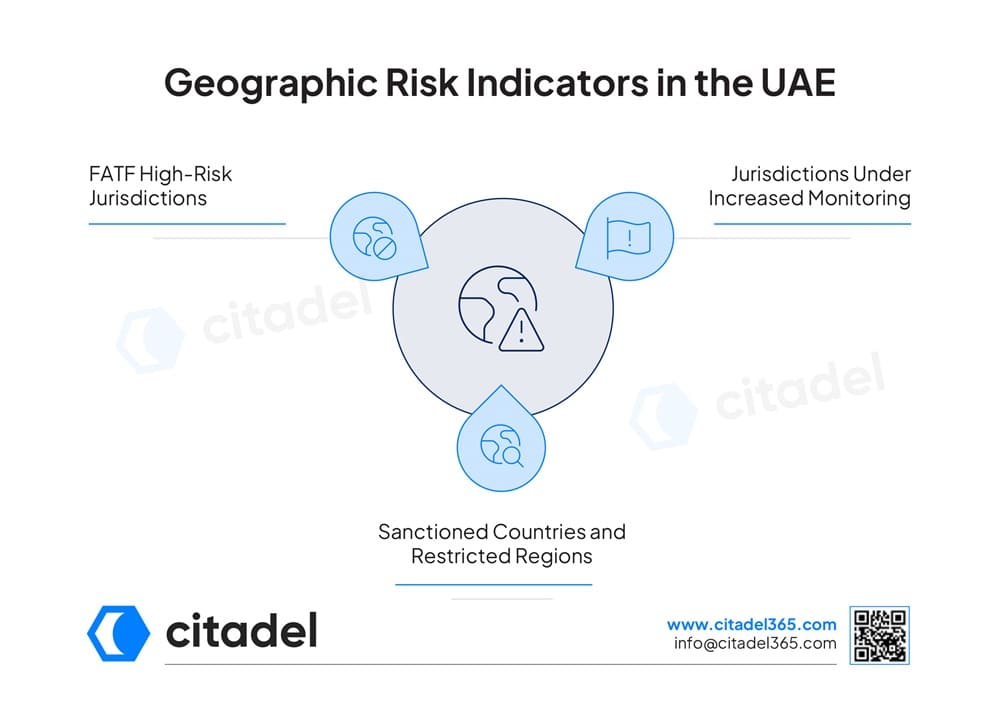

Geographic risk is a key element of Customer Risk Assessments (CRAs) under UAE AML regulations. A customer’s business relationships with certain countries or regions can significantly increase the customer’s exposure to the risks of money laundering, terrorist financing, sanctions violations, corruption or other financial crime.

When assessing customer risk, regulated entities should not only consider where a customer lives or is incorporated, but also the countries involved with the customer’s business activities, ownership structures, source of funds, transaction flows and counterparties. Geographic exposure is frequently not evaluated on its own and should be viewed in conjunction with other risk factors to establish the overall risk profile of the customer.

FATF High-Risk Jurisdictions

The Financial Action Task Force (FATF) lists jurisdictions with serious deficiencies in their Anti-Money Laundering and Counter-Terrorist Financing (AML/CFT) regimes. These jurisdictions are commonly known as “High-Risk Jurisdictions Subject to a Call for Action”. The FATF “blacklist” is a list of countries with the most serious cases.

A customer can be exposed to such jurisdictions through:

Customers connected to such jurisdictions are subject to higher AML risks as local regulatory controls may not be adequate to detect and prevent financial crime. The FATF requires members to take certain countermeasures to safeguard the global financial system from the elevated risk of money laundering, terrorist financing and proliferation financing in these cases.

Jurisdictions Under Increased Monitoring

FATF also publishes a list of countries under Increased Monitoring. This list is often called the “grey list”. These jurisdictions have made a formal commitment to work with the FATF and relevant regional bodies to address deficiencies in their AML/CFT measures within agreed timeframes and are subject to ongoing monitoring.

A country being on the grey list doesn’t automatically mean that it is highly susceptible to financial crime, but it is an indicator of potential vulnerabilities that should be considered in customer risk assessments.

Organisations need to assess the customer’s relationship with the jurisdiction, the sort of dealings, the effectiveness of AML controls for risk mitigation and other customer-related risk factors. Customers located in jurisdictions under increased monitoring may be subject to further due diligence and ongoing monitoring, depending on the overall risk profile.

Sanctioned Countries and Restricted Regions

Customers who have ties to sanctioned countries, territories, entities or individuals present significant compliance risks. The UAE or other competent international authorities may impose sanctions that may restrict financial transactions, business relationships and economic activities as determined by the United Nations Security Council (UNSC).

Organisations should evaluate whether customers are:

Failure to identify sanctions exposure may lead to regulatory penalties, reputational damage, and possible AML and sanctions compliance violations. Therefore, sanctions screening should be an integral part of the customer onboarding and ongoing monitoring processes.

How Geographic Exposure Influences Risk Ratings

Geographic risk is assessed based on the customer’s overall global exposure rather than relying solely on the country of residence or incorporation. Various geographic touchpoints are considered before assigning the final risk rating to a customer.

Factors typically considered by organisations include:

Where a customer has significant exposure to high-risk jurisdictions, the risk rating may be higher, and the customer may be subject to Enhanced Due Diligence (EDD), additional verification requirements and increased monitoring.

However, geographic exposure should always be considered as part of a wider risk-based approach. The final risk classification of a customer should take into account the cumulative effects of the various types of risk factors, such as geographic, customer, ownership, transactional and behavioural risk factors, for an overall and proportionate AML risk assessment.

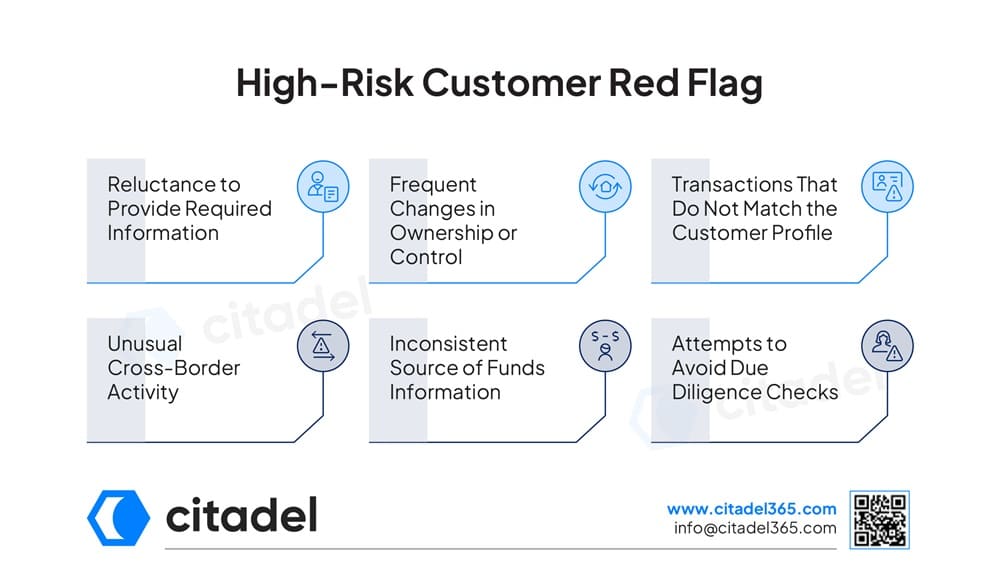

Customer risk assessments are based on a number of risk factors, however, there are some warning signs or red flags that may indicate that a customer presents an elevated risk of money laundering, terrorist financing, sanctions evasion, or other financial crimes. These indicators do not necessarily indicate illicit activity, but may warrant further investigation, enhanced due diligence, and a re-evaluation of the customer’s risk rating. Early detection of red flags helps organisations to tighten their AML controls, identify suspicious activities and ensure compliance with the regulatory requirements in the UAE.

Reluctance to Provide Required Information

Customers who refuse or are reluctant to provide information required for Customer Due Diligence (CDD) purposes may pose a higher AML risk. Failure to provide identification documents, refusal to provide information on beneficial ownership, incomplete responses, or failure to cooperate or refusal to provide source of funds information may be an attempt to conceal important information about the customer or the nature of the business relationship. Such behaviour should trigger further verification and enhanced scrutiny during onboarding and ongoing monitoring.

Frequent Changes in Ownership or Control

Frequent changes in ownership, management, authorised signatories or control structures may indicate attempts to conceal the true ownership of a business. There may be legitimate commercial reasons for ownership changes, but multiple or unexplained changes over short periods may hinder the identification of the ultimate beneficial owner and could indicate an attempt to avoid regulatory scrutiny. Organisations need to carefully consider the reasons for such changes and reassess the customer’s risk profile where necessary.

Transactions That Do Not Match the Customer Profile

The transaction activity of a customer should generally be consistent with the customer’s known business activities, expected account activity and financial profile. Higher risk transactions are those that are significantly above normal transaction volumes, involve unusual counterparties or have no apparent commercial purpose. Any sudden change in transaction patterns or activity which appears inconsistent with the customer’s occupation, industry or business model should be investigated to determine whether there are additional due diligence or reporting obligations.

Unusual Cross-Border Activity

International transactions are common in the global economy today, but unusual or unexplained cross-border activity can heighten AML risks. People who regularly send money to entities abroad with which they have no connection, who conduct business in high-risk countries or transfer funds across multiple countries without a reasonable business explanation may find themselves under additional scrutiny. Sometimes, activity like this can be used to hide the source, ownership, or destination of funds. These should be assessed thoroughly based on the customer’s overall risk profile.

Inconsistent Source of Funds Information

Customers should be able to give a clear and consistent explanation about the source of their funds and wealth. The customer’s information might be inconsistent with supporting documents or might change over time without a reasonable justification. This may suggest an increased risk of money laundering. Inconsistent explanations, unsupported claims of wealth accumulation or inability to provide explanations for large amounts of financial activity should trigger additional investigation and verification.

Attempts to Avoid Due Diligence Checks

Customers seeking to avoid or reduce due diligence processes may represent a higher compliance risk. This could involve putting pressure on staff to speed up the onboarding process, withholding requested documents, using third parties to avoid direct verification, or arranging relationships in a way that hides who the real owners are. Such behaviour could require a lack of transparency and could require Enhanced Due Diligence (EDD), escalation to compliance teams, and ongoing monitoring.

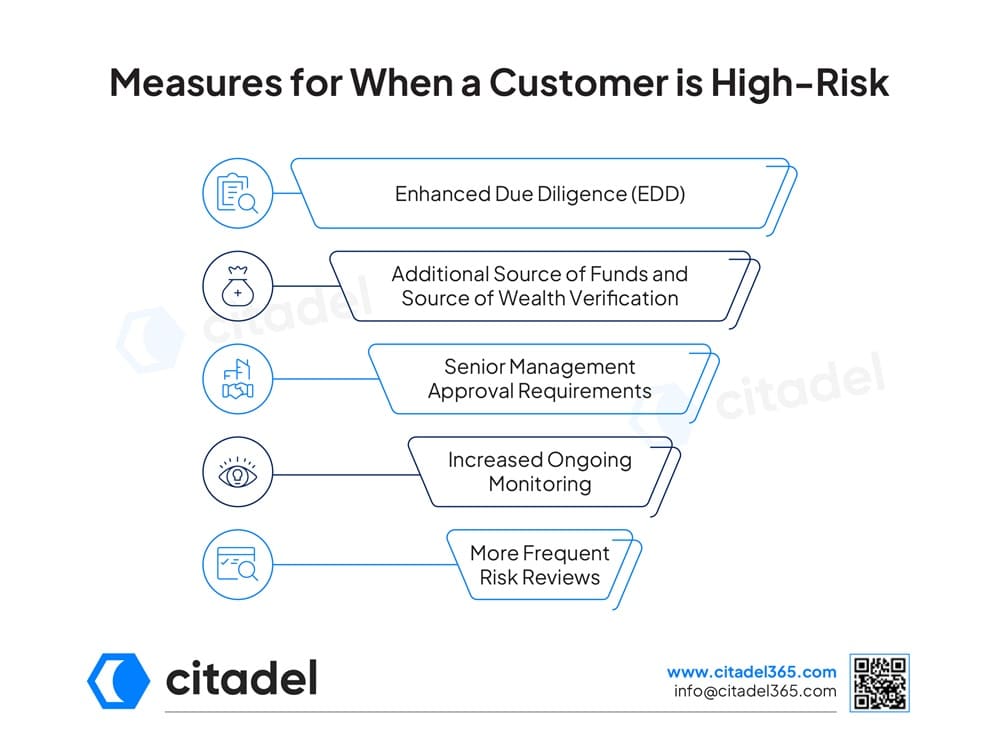

High-risk customers require enhanced controls and monitoring measures by organisations to address increased exposure to money laundering, terrorist financing, sanctions violations, or other financial crime risks. It is important to note that a high-risk rating does not imply that a customer is involved in illegal activity as per the UAE AML regulations. Instead, it signals a need for greater scrutiny and an improved set of risk mitigation measures throughout the customer relationship lifecycle.

Enhanced Due Diligence (EDD)

Enhanced Due Diligence (EDD) is one of the key measures applied to high-risk customers. Standard Customer Due Diligence (CDD) is the process of verifying the identity of the customer and understanding the nature of the relationship. Enhanced Due Diligence (EDD) is a more detailed assessment of the customer’s background, business activities, ownership structure and risk factors.

Additional Source of Funds and Source of Wealth Verification

High-risk customers may require increased levels of verification of the source of funds and the source of wealth. Source of funds is the origin of the money in a particular transaction or business relationship; source of wealth is the way in which the customer has accumulated his/her overall assets and financial resources.

Senior Management Approval Requirements

In certain high-risk customer relationships, particularly those including PEPs or other high-risk factors, organisations may be required to obtain senior management approval in specific circumstances before entering into or continuing a business relationship.

Increased Ongoing Monitoring

High-risk customers are generally subject to more intensive ongoing monitoring than standard-risk customers. This means looking more closely at transactions, customer activities and behavioural patterns to spot unusual or potentially suspicious activity.

Monitoring programs may include transaction volumes, payment destinations, geographic exposure, changes in account activity and other risk indicators. The objective is to be able to identify new risks as quickly as possible and to ensure that the customer’s activity corresponds to their known profile and expected business behaviour.

More Frequent Risk Reviews

Once a customer has been classified as high risk, a customer risk assessment should not be a static exercise. Instead, organisations should review more frequently to make sure the customer’s risk profile is accurate and up to date.

Periodic reviews help to identify changes such as new business activities, changes in ownership, adverse media findings, sanctions exposure, changes in geographic risk or unusual transaction behaviour. Ongoing assessment of high-risk customers enables organisations to assess the need for additional controls, a change in risk rating or further investigation.

Accurate identification of high-risk customers is crucial to effective AML compliance programs. However, many organisations make mistakes that can lead to inaccurate risk assessments, inadequate due diligence, and increased exposure to financial crime risks. Knowing such common mistakes can help businesses to improve the customer risk assessment processes and get better compliance outcomes.

Treating Risk Assessments as a One-Time Exercise

One of the biggest mistakes companies make is to treat customer risk assessments as a one-and-done activity during onboarding. Over time, customer risk profiles can change significantly due to changes in ownership, business activities, geographic exposure, transaction patterns or regulatory developments. A customer that is classified as low or medium risk may become high risk as new information comes to light. A good AML program understands that customer risk assessment is an ongoing process that includes continuous monitoring and periodic reviews throughout the customer lifecycle.

Over-Reliance on Country Risk Alone

Geographic exposure is a major consideration in AML risk assessments, country risk alone can be a poor predictor of customer classification. A customer in a higher risk jurisdiction may still be an acceptable level of risk when other factors are taken into account, while a customer in a lower risk jurisdiction may have behaviours or ownership structures that should place it in a higher risk category. To develop a balanced and comprehensive assessment, organisations should consider country risk in the context of customer characteristics, transaction activity, beneficial ownership information, source of funds and other relevant risk indicators.

Ignoring Beneficial Ownership Risks

A major weakness in many customer risk assessment programs is the failure to adequately identify and verify beneficial ownership. Individuals who ultimately own or control an entity may use complex corporate structures, nominee arrangements and layered ownership models to hide themselves. Entities that rely only on legal ownership and do not understand who actually controls them may miss important AML risks. Verification of beneficial ownership should be an integral part of customer due diligence and risk assessment processes, in particular for corporate customers and legal arrangements.

Failing to Reassess Customers When Circumstances Change

Customer risk ratings should be reassessed whenever there are significant changes affecting the customer’s risk profile. Companies may not reassess risk classifications after events such as changes in ownership structures, entry into higher-risk markets, unusual transaction activity, negative media coverage or new sanctions and PEP screening results. If the reassessment is not done on time, the organisation may continue to use controls that are outdated and do not reflect the real level of risk of the customer. Trigger-based reviews are critical for keeping risk ratings accurate and effective.

Poor Documentation of Risk Decisions

Poor documentation can cause major compliance problems even with thorough risk assessments. Regulators want firms to explain how they reached customer risk ratings, what information they used and why certain due diligence measures were used. Poor recordkeeping makes it difficult to justify risk classifications, support compliance decisions during audits, and demonstrate adherence to AML requirements. Documentation that is clear, consistent and audit-ready helps to ensure transparency, accountability and regulatory compliance throughout the customer risk assessment process.

Citadel365 helps organisations better manage high-risk customers by automating key compliance processes and providing greater visibility into changing customer risk. It offers a single platform for customer risk assessment, screening, monitoring and case management, enabling compliance teams to make more informed, risk-based decisions more efficiently.

Organisations can leverage Citadel365 to develop dynamic customer risk profiles by integrating key risk factors such as customer type, geographical exposure, beneficial ownership data, PEP status, sanctions screening results, source of funds information and transaction behaviour into a common risk assessment platform. As new information becomes available, customer profiles can be automatically updated based on available data sources and configured workflows, providing compliance teams with an always-accurate, complete view of the customer’s risk exposure.

Citadel365 automates the customer risk rating process through configurable risk-scoring methodologies that can be defined to meet the organisation’s AML policies and regulatory requirements.

The platform assesses multiple risk indicators in parallel and automatically assigns customer risk ratings based on pre-defined rules and risk models. This helps provide consistency across the organisation, reduces manual effort, and allows compliance teams to focus their attention on higher-risk areas.

Citadel365 automated workflows provide structured processes for collecting supporting documentation, risk reviews, task assignments, case escalations and recording approval decisions. This allows organisations to uniformly implement necessary due diligence processes and maintain transparent documentation for all compliance efforts.

Citadel365 offers continuous customer risk monitoring capabilities, enabling organisations to identify material risk changes in real-time. Compliance teams can use automated alerts, trigger-based reviews and continuous screening to rapidly reassess customer risk ratings and implement additional controls where required. This helps keep risk assessments updated across the entire customer lifecycle.

Citadel365 offers a complete audit trail of customer risk assessments and compliance activities, ensuring that all actions, decisions and supporting evidence are properly recorded and easily accessible, enhancing transparency and streamlining audit and regulatory review processes.

No, a high-risk customer does not automatically indicate money laundering. It simply indicates a higher potential risk, requiring enhanced due diligence (EDD) and ongoing monitoring.

Yes, because AML risk is dynamic due to changes in ownership, business activities, transaction patterns, geographic exposure, or sanctions/PEP status, which can increase a customer’s risk level.

High-risk customers require enhanced due diligence (EDD), where necessary, including identity verification, source of funds and source of wealth checks, and ongoing monitoring.

Yes, businesses can assign different risk ratings based on each customer’s profile, including ownership structure, transaction behaviour, geographic location, and other risk factors.

Arjun is the Co-founder and CEO of Citadel, where he leads the company’s vision across technology, business, and regulations. He brings over a decade of experience in building and scaling technology ventures. Arjun holds a B.Tech. in Information Technology and a Master’s in Management, supported by his certification as a Financial Crime Specialist, an uncommon combination that allows him to balance innovation with regulatory requirements.

Having advised leading banks and financial institutions on digital solutions and compliance technology, Citadel continues to grow with an ambition.