Ready to Defeat Your AML Compliance Obstacles?

Citadel Brings Revolution with Secure Solutions to AML Compliance Problems

AML/CFT policies and procedures are a set of rules that define an organisation’s approach to identifying, managing and mitigating money laundering, terrorist financing, and proliferation financing risks.

Every regulated entity requires documented AML controls, as they provide clarity, consistency, and accountability. Policies and procedures serve as evidence that showcase a business understands its ML/TF and other financial crime risks and has implemented required measures to prevent them.

The core difference between policies, procedures, and internal controls is:

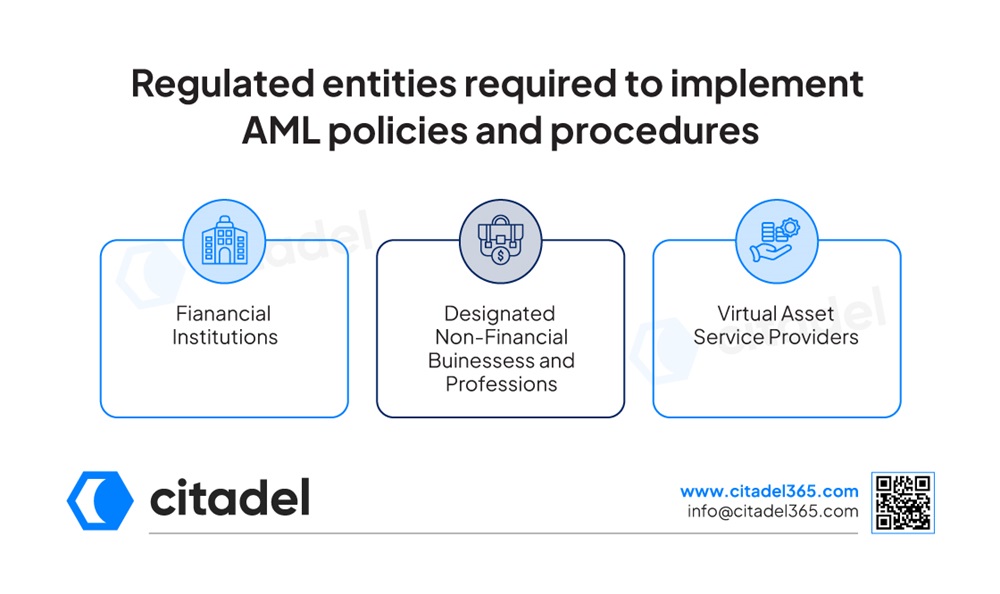

AML obligations extend across a broad spectrum of regulated sectors within the UAE. The following are the regulated entities that are required to implement AML policies and procedures:

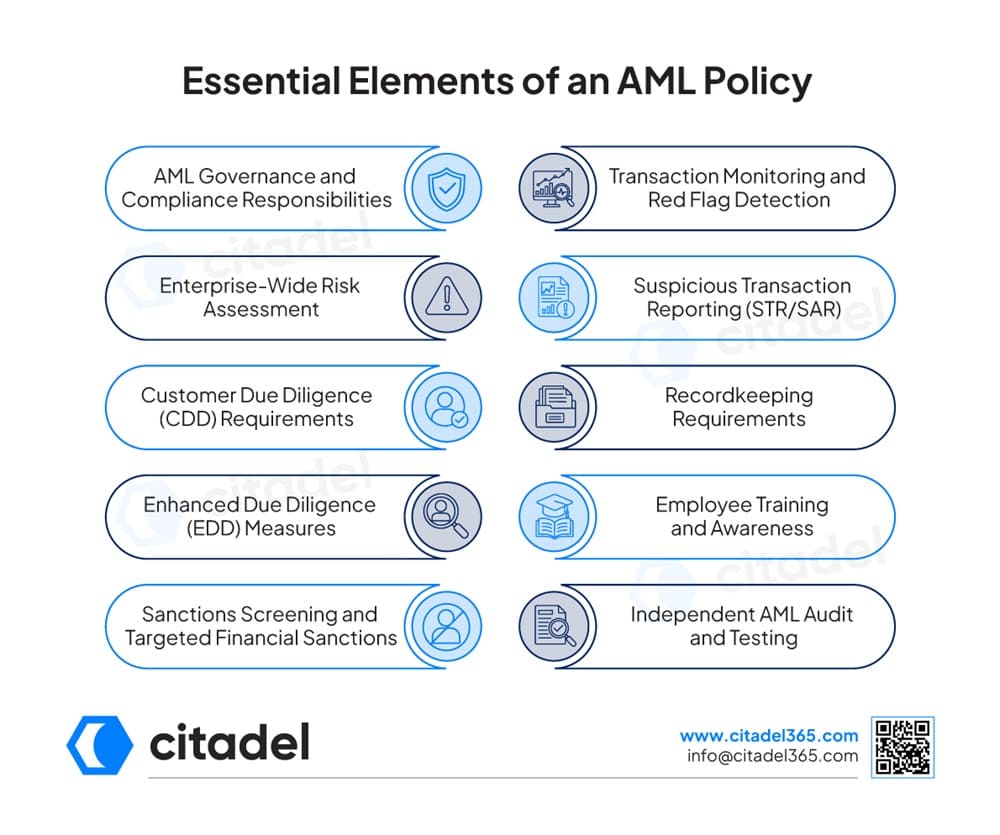

Behind every effective AML programme lies a well-defined AML policy framework that provides a blueprint for managing ML/TF risks, while ensuring consistency, accountability, and regulatory compliance.

An AML policy should include governance and compliance responsibilities, ensuring the firm’s commitment towards combating money laundering and other financial crime.

EWRA works as a critical component, helping organisations to identify, assess, and manage ML/TF risks across the business.

CDD enables verifying, identifying, and assessing the customer risk levels and ensures ongoing monitoring of customer transactions, preventing ML/TF risk.

EDD helps specify additional verification and monitoring requirements for customers and transactions that present elevated ML/TF risk.

It set out procedures for customer and transaction screening against the relevant sanctions lists and ensuring regulatory compliance with targeted financial sanctions requirements.

AML policy should also include transaction monitoring to identify key red flags, including unusual patterns that may indicate money laundering.

Providing clear procedures for escalating, investigating, and reporting the suspicious transaction report and suspicious activity report to the relevant authorities.

Defines the types of records that must be maintained and retained, including transaction records or customer identification documents to support regulatory investigations and compliance requirements.

Ensuring a staff training and awareness programme for employees to understand their responsibilities and recognise ML/TF risk under the AML policy.

It helps in periodic independent reviews to assess the effectiveness of AML policies, procedures, and internal controls.

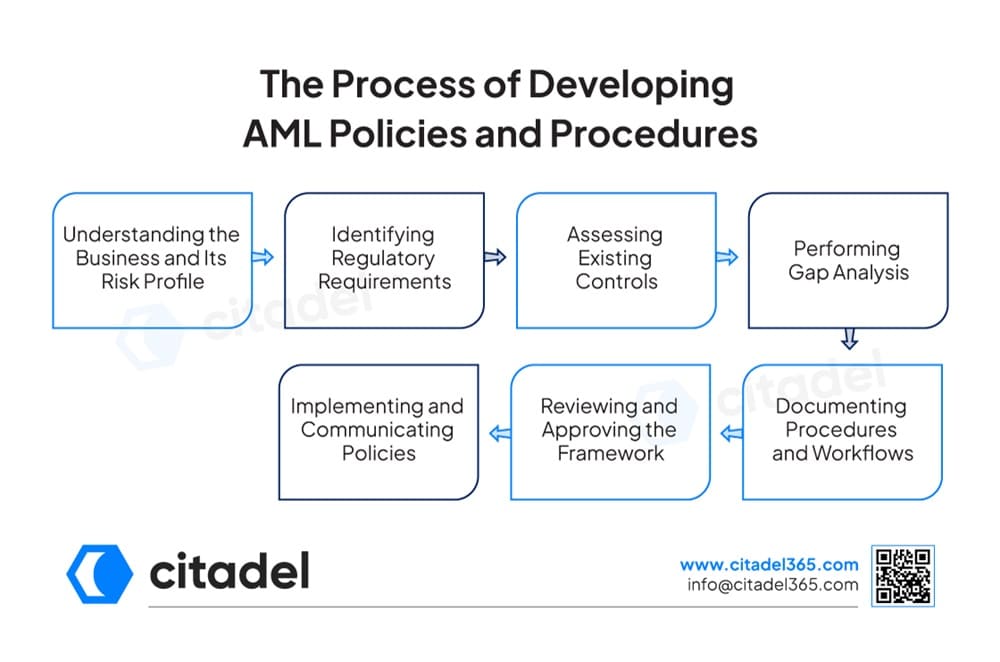

Much like a perfect blueprint guides the construction of a secure building, AML policies and procedures provide a framework for managing ML/TF risks. Policy development transforms regulatory requirements into practical controls, creating a defensible and operationally effective compliance framework.

Understanding the Business and Its Risk Profile

Developing policies and procedures involves understanding the business and its risk profile, including conducting a risk assessment to identify and evaluate potential ML/TF risk.

Identifying Regulatory Requirements

Identifying key AML laws, regulations, and industry-specific obligations applicable to the business, ensuring that policies and procedures are well-aligned with regulatory requirements.

Assessing Existing Controls

Assessing current AML measures, governance structures, and compliance processes for ensuring the effectiveness of compliance frameworks.

Performing Gap Analysis

Policy development also includes conducting a gap analysis to identify AML deficiencies between pre-existing controls and regulatory expectations and recommending the required measures to address them.

Documenting Procedures and Workflows

Crafting clear operational procedures and workflows that support the practical implementation of AML policies during regulatory investigations.

Reviewing and Approving the Framework

Conducting a review and obtaining senior management approval to ensure the accuracy and effectiveness of the framework.

Implementing and Communicating Policies

Implementing the AML policies across the organisation and ensuring employees understand their compliance responsibilities.

Businesses struggle with AML policy implementation due to several key challenges:

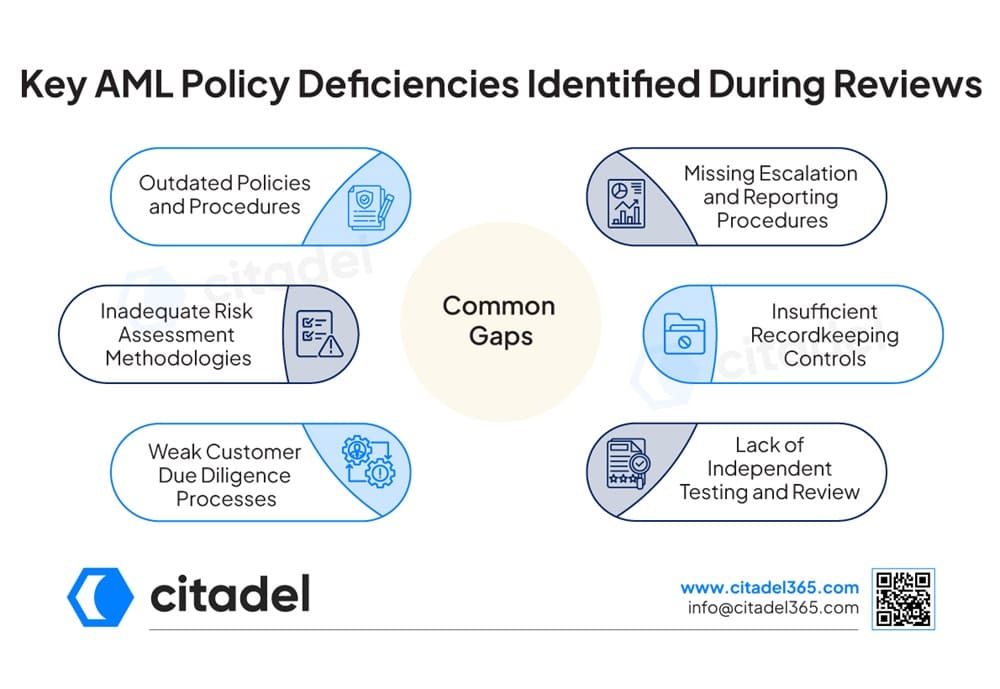

AML policy reviews often reveal weaknesses that reduce the effectiveness of compliance frameworks and increase the regulatory exposure. The common gaps identified during the AML policy review are as follows:

Outdated Policies and Procedures

Policies that are not updated on a regular basis may fail to reflect current regulatory requirements and emerging risks, often creating gaps in the AML framework.

Inadequate Risk Assessment Methodologies

Inadequate or incomplete risk assessment frameworks result in inaccurate risk identification, ineffective allocation of AML controls, and increased ML/TF risks.

Weak Customer Due Diligence Processes

Weaknesses in customer verification, risk assessment, or ongoing monitoring procedures increase the ML/TF risk exposure.

Missing Escalation and Reporting Procedures

Delays in filing suspicious activity reports and ineffective escalation processes are the common issues.

Insufficient Recordkeeping Controls

Poor record-keeping controls and documentation practices can lead to compliance gaps and hinder regulatory investigations or audits.

Lack of Independent Testing and Review

Without independent reviews and testing, organisations may struggle to identify gaps in their AML policies, procedures, and internal controls.

Effective policies and procedures build the foundation of a strong compliance framework. Citadel365 helps businesses develop tailored compliance AML/CFT policies, procedures, and compliance frameworks that align controls with your business risks, which help in improving consistency across business operations and supporting compliance with the UAE’s evolving regulatory requirements.

Citadel365 develops AML/CFT policies and procedures for the full range of regulated entities in the UAE: banks and financial institutions, lawyers, notaries and other legal professionals, accountants and auditors, dealers in precious metals and stones, real estate agents, money services businesses, virtual asset service providers, corporate service providers, and other regulated businesses.

Every framework we draft reflects the latest UAE AML/CFT laws and regulations, including Federal Decree-Law No. 10 of 2025 and Cabinet Resolution No. 134 of 2025, together with the applicable supervisory guidelines. We also factor in the findings of the UAE National Risk Assessment (NRA) and Sectoral Risk Assessments (SRA) and global best practices, so your policies stay aligned with both regulatory expectations and your actual risk exposure.

Citadel365’s approach helps strengthen governance and accountability, enhance regulatory readiness, and support sustainable compliance programmes.

AML policies and procedures are documented guidelines that outline how businesses identify, manage, and mitigate ML/TF/PF risks.

An AML policy should include governance responsibilities, risk assessment, customer due diligence, transaction monitoring, sanctions screening, reporting, record-keeping, and independent testing.

As a best practice, businesses should conduct a review of their AML policy at least annually and whenever there is a significant change to regulatory requirements, business activities, or ML/TF risk exposure.

AML policies define what businesses must do to prevent ML/TF risks, whereas AML procedures describe how those policies are effectively implemented in daily business operations.

Risk-based approach is crucial while drafting AML policies because it allows organisations to allocate resources effectively based on their risk level and apply appropriate controls to high-risk areas.

Arjun is the Co-founder and CEO of Citadel, where he leads the company’s vision across technology, business, and regulations. He brings over a decade of experience in building and scaling technology ventures. Arjun holds a B.Tech. in Information Technology and a Master’s in Management, supported by his certification as a Financial Crime Specialist, an uncommon combination that allows him to balance innovation with regulatory requirements.

Having advised leading banks and financial institutions on digital solutions and compliance technology, Citadel continues to grow with an ambition.