Ready to Defeat Your AML Compliance Obstacles?

Citadel Brings Revolution with Secure Solutions to AML Compliance Problems

Enterprise-Wide Risk Assessment enables regulated entities to identify, assess, and mitigate money laundering and terrorist financing (ML/TF) risks. It helps entities understand their ML/TF vulnerabilities and develop a potential strategy to mitigate compliance risks. EWRA is the foundation for regulated entities’ policies, procedures, and controls.

Enterprise-Wide Risk Assessment is also known as ML/FT risk assessment, Business Risk Assessment, Firm-Wide Risk Assessment, Entity-Risk Assessment, Practice-Wide Risk Assessment, Institutional Risk Assessment, or Business-Wide Risk Assessment.

EWRA is a mandatory obligation for Financial Institutions and Designated Non-Financial Businesses and Professions (DNFBPs) and VASPs in the UAE. Cabinet Resolution No. 134 of 2025 requires these DNFBPs, Financial Institutions, and VASPs to understand their ML/TF risks and take necessary steps to manage those risks by adopting a risk-based approach.

Financial institutions include banks, exchange houses, insurance companies, securities, and investment firms. DNFBPs include real estate brokers and agents, auditors & independent accountants, lawyers & legal professionals, company service providers, dealers in precious metals and stones (DPMS), commercial gaming operators, and other DNFBPs, who are exposed to financial crime risks and required to carry out EWRA.

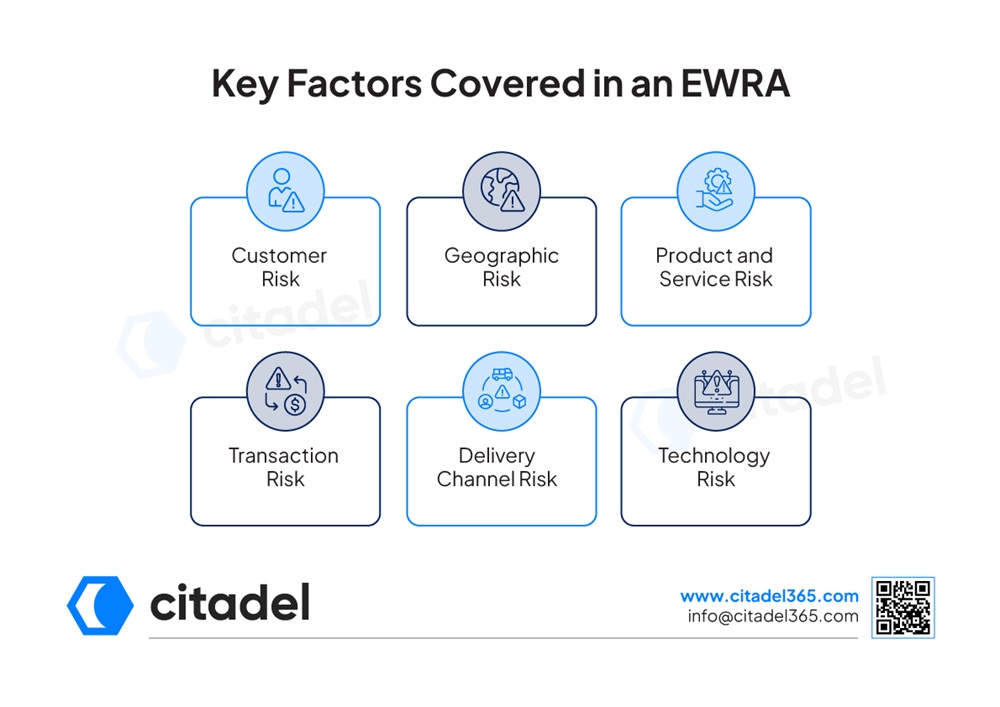

Conducting an Enterprise-Wide Risk Assessment in the UAE for regulated entities should cover the following:

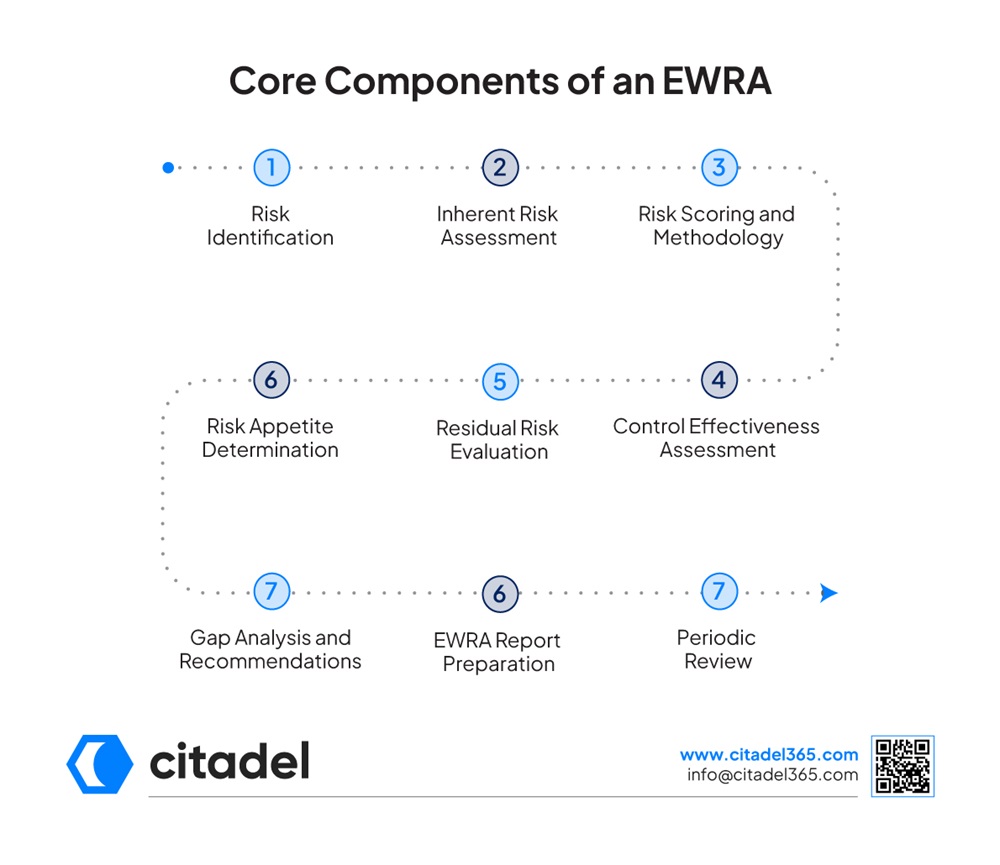

EWRA includes the following key components:

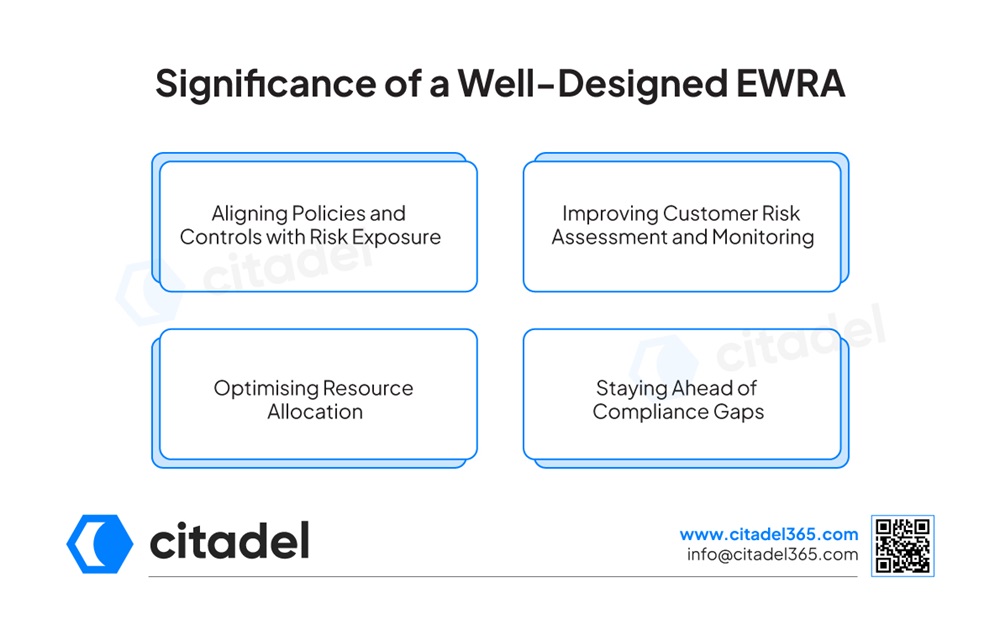

Enterprise-Wide Risk Assessment forms the foundation for constructing an effective AML/CFT program. The following points provide the significance of a well-designed EWRA:

Aligning Policies and Controls with Risk Exposure

EWRA helps identify ML/TF vulnerabilities that exist and helps develop tailored policies, procedures and controls to mitigate or manage the identified risks, ensuring alignment of policies & controls with the entity’s ML/TF risk exposure.

Improving Customer Risk Assessment and Monitoring

EWRA acts as a guide for KYC, risk assessment, and monitoring systems to function in practice. It ensures entities adopt a risk-based approach to apply customer risk assessment and monitoring, with increased scrutiny for high-risk customers and transactions.

Optimising Resource Allocation

A well-designed EWRA provides an absolute picture of the organisation’s exposure to ML/TF risks and ensures efficient allocation of resources. It helps regulated entities prioritise high-risk areas and plan risk management efforts.

Staying Ahead of Compliance Gaps

EWRA systematically maps out potential ML/TF risks and prioritises risk mitigation. The complete process helps compare the existing controls with the actual risk and further calculate the residual risks. It further helps align risk with the business risk appetite and apply relevant controls, thereby helping mitigate compliance gaps before regulators do.

Businesses face the following challenges when conducting EWRA:

Identifying Relevant Risk Factors

It is important to consider various risk factors, such as customers, products, transactions, geographies, and delivery channels, while conducting EWRA. Entities often find it difficult to identify relevant risk factors, especially when operating across diverse lines of business.

Quantifying Inherent and Residual Risks

Assessing risks before and after the controls applied is often challenging, as some risks cannot be measured exactly.

Assessing the Effectiveness of Controls

EWRA involves evaluating the existing controls, which require review of policies, procedures and compliance measures. Entities often struggle to assess the effectiveness of existing controls, leaving gaps in the developing control framework.

Aligning EWRA with Regulatory Expectations

Regulators expect a risk-based approach, instead of generic templates. Further, with evolving guidance, it is difficult for entities to meet the expectations.

Maintaining Consistency Across Business Units

Regulated entities with multiple departments or branches must use the same approach across all. Maintaining consistency across all units using the same risk-scoring approach can be challenging.

Keeping the Assessment Up to Date

Regulated entities need to update EWRA periodically and when launching new products, adopting new technologies or operating in new jurisdictions. Keeping the EWRA up to date with significant updates can be challenging.

Regulated entities often make the following mistakes when conducting an Enterprise-Wide Risk Assessment:

Citadel365 provides EWRA Services in the UAE to help regulated entities meet regulatory requirements and enhance their AML/CFT compliance framework. The team with regulatory expertise has a thorough understanding of UAE AML regulations, helping entities align with supervisory expectations.

Further, the industry-specific risk knowledge helps design an accurate business risk assessment. Citalde365 uses tailored risk methodologies instead of relying on generic templates, to include various risk factors such as customers, services, products and geographic exposure.

Citadel365 EWRA services include practical risk mitigation recommendations that help regulated entities strengthen their controls. Additionally, Citadel365 provides support beyond the EWRA report, including implementing measures and designing effective policies and procedures to ensure AML/CFT compliance.

An enterprise-wide risk assessment (EWRA) is a comprehensive process for identifying, assessing, and mitigating the ML/TF risks an organisation faces. It is a foundation for the organisation’s risk management and AML/CFT compliance program.

Inherent risk is the raw risk that is present in the organisation before any controls are applied. Residual risk is the remaining risk after existing controls are put in place. EWRA helps calculate inherent and residual risks.

Standard or generic templates do not fit all types, natures, and sizes of businesses. Regulatory authorities require entities to adopt a tailored risk-based approach to design EWRA, specific to the business nature, size, and complexity.

EWRA helps identify, evaluate and prioritise a business’s exposure to financial crime, drawing on factors such as customers, products, services, delivery channels, and geographies, helping organisations move from a tick box approach to a risk-based approach.

Professional EWRA services help businesses align compliance measures with AML/CFT regulatory requirements, design industry-specific tailored risk assessments, and adopt a risk-based approach, ensuring that resources are invested where required.

Arjun is the Co-founder and CEO of Citadel, where he leads the company’s vision across technology, business, and regulations. He brings over a decade of experience in building and scaling technology ventures. Arjun holds a B.Tech. in Information Technology and a Master’s in Management, supported by his certification as a Financial Crime Specialist, an uncommon combination that allows him to balance innovation with regulatory requirements.

Having advised leading banks and financial institutions on digital solutions and compliance technology, Citadel continues to grow with an ambition.